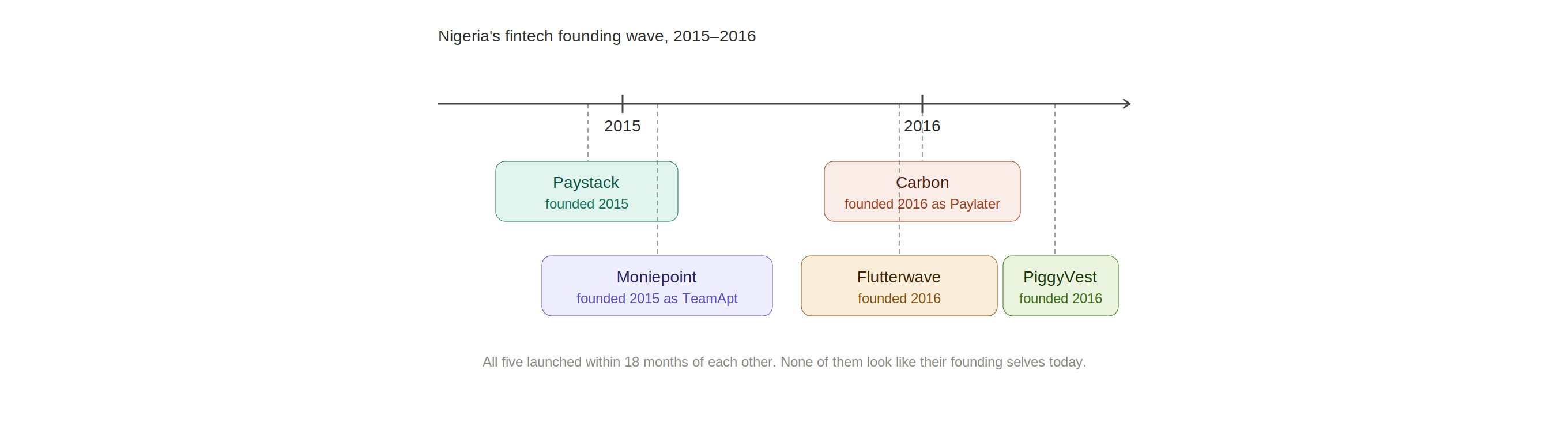

Nigeria’s fintech class of 2015-2016 turns 10 | Here is what a decade built

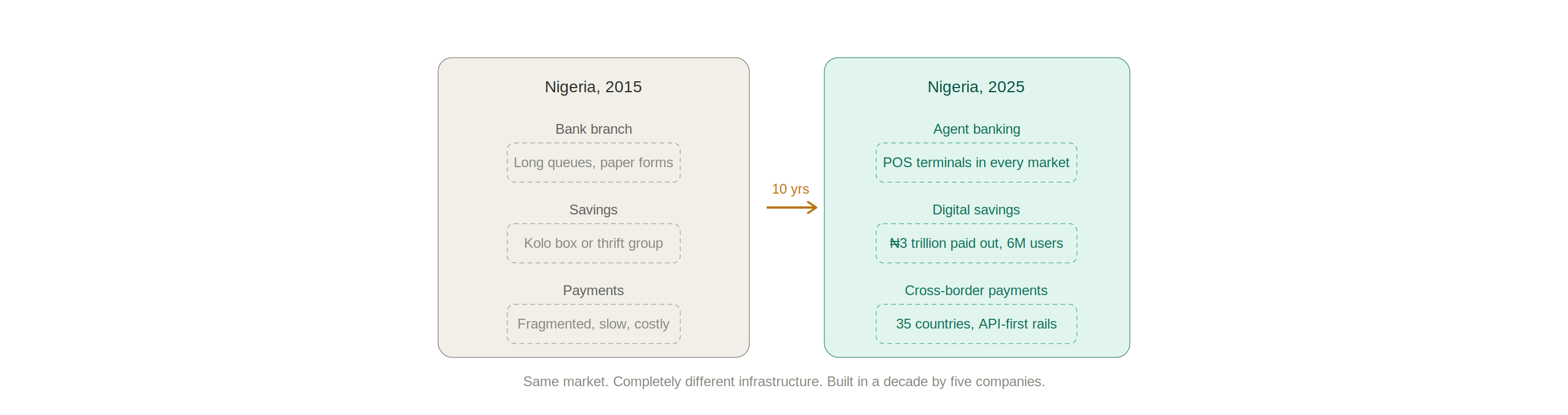

Ten years is a long time in Nigerian fintech. Long enough to go from a pitch deck to a billion-dollar valuation. Long enough to watch a rebrand become a company-wide identity shift. Long enough to see a simple savings app accumulate more than ₦3 trillion in lifetime payouts.

In 2025 and 2026, five companies that launched between 2015 and 2016 are marking a decade in operation: Paystack, Moniepoint, Flutterwave, Carbon, and PiggyVest.

Their anniversaries land at different points, and their trajectories diverged sharply, but their survival alone is worth examining in a market where most startups do not make it past year three.

None of them started where they ended up.

Paystack, founded by Shola Akinlade and Ezra Olubi in 2015 and publicly launched in January 2016, set out to make online payments work cleanly for Nigerian merchants. It did that well enough that Stripe acquired it in 2020 for a reported $200 million, the largest acquisition of an African tech startup at the time.

The acquisition removed Paystack from the independent fundraising race but did not slow its product velocity. The launch of Zap, a real-time transfer product targeting sub-10-second bank transfers, signalled that Paystack was still building for speed and reliability in its home market even under a global parent. And recently, it all became The Stack Group.

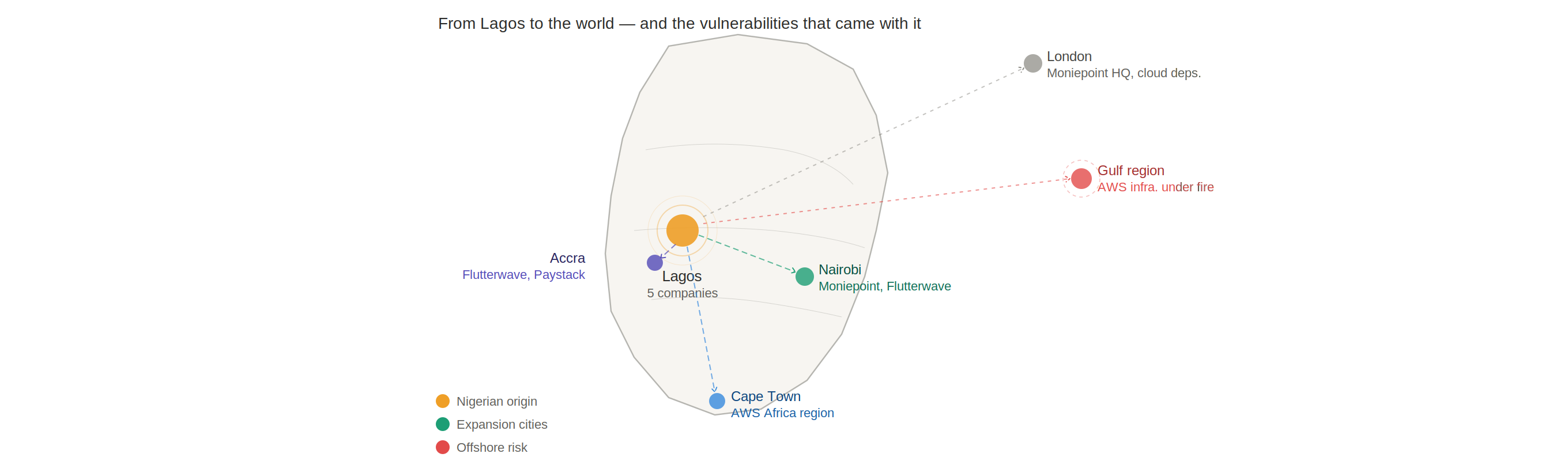

Flutterwave, co-founded by Olugbenga Agboola and Iyinoluwa Aboyeji in 2016, had a different ambition from the start. Where Paystack optimised for Nigerian merchant simplicity, Flutterwave built infrastructure for cross-border complexity, API-first payments that could handle multiple currencies, settlement protocols, and regulatory requirements across 35 countries simultaneously.

That ambition took it to unicorn status in 2021 after a $170 million Series C, and to a $3 billion valuation after a $250 million Series D in 2022. By January 2026, Flutterwave had acquired Mono, a Nigerian open-banking infrastructure provider, folding account-linking and financial data capabilities directly into its payments stack.

Moniepoint’s decade is the most structurally interesting of the five. Founded as TeamApt in June 2015 by Tosin Eniolorunda and Felix Ike, it spent its first four years as a backend provider, building core banking software and API integrations for financial institutions. Most Nigerians had never heard of it. The 2019 pivot changed that.

The company built an agency banking network, pushed blue-and-white POS terminals into markets, motor parks, and roadside shops across the country, and quietly became the largest business payments platform in Nigeria by transaction volume.

By 2023, it had rebranded to Moniepoint, entered consumer banking, and raised its way to unicorn status. In March 2026, it acquired Orda Africa. Its tenth year found it in Kenya, having secured a majority stake in Sumac Microfinance Bank, the kind of international footprint it would have been hard to imagine for a company that spent its first four years invisible to most of the market it now dominates.

Carbon launched in March 2016 as Paylater, a consumer lending app built on the premise that Nigerians with smartphones and bank accounts deserved fast, collateral-free credit. It was one of the earliest Nigerian fintechs to tackle credit scoring algorithmically rather than through traditional bank gatekeeping.

The company rebranded to Carbon in 2019 and expanded into payments, savings, and business banking. Its tenth year arrives quietly, without the unicorn narrative or the Stripe-level exit, but Carbon’s early credit infrastructure work shaped how the broader ecosystem thought about digital lending, and its persistence through multiple product evolutions is its own kind of durability.

PiggyVest is the outlier in this group in the best possible way. Founded in 2016 as Piggybank.ng, it built a product that did one thing: help Nigerians save money by making withdrawal deliberately difficult. That constraint, which many early users found annoying, turned out to be the entire value proposition.

In 2025, it paid out ₦1.3 trillion to users, a 56% increase on the previous year, and crossed six million registered accounts. Its assets under management doubled in 2025, growing 110%. The company announced its tenth anniversary celebrations in April 2026, with co-founder Joshua Chibueze hinting at a 10,000-seat venue for its Lagos OpenHouse event. That is a signal that PiggyVest has built something most Nigerian fintechs have not: a user base that shows up.

What survival actually required

The 2015-2016 cohort launched into a Nigeria where mobile internet penetration was growing but still uneven, where the CBN was still working out its framework for payment service providers, and where the dominant mental model for savings was a physical kolo or a bank branch.

All five companies bet that software could do what institutions had not. That bet paid off, but it required more than a good product. It required regulatory navigation. Every company in this cohort had to earn licences, negotiate with the CBN, and in some cases absorb policy reversals that changed their cost structure overnight.

Flutterwave secured Nigeria’s switching and processing licence in 2022, the highest-tier CBN payment licence, which allowed it to process transactions between banks and cards without intermediaries.

Moniepoint’s 2019 switching licence from the CBN was the turning point that unlocked its agency banking ambitions. The regulatory relationship was never easy, but it was unavoidable, and the companies that treated compliance as infrastructure rather than a tax on growth lasted.

It needed the ability to pivot without losing identity. TeamApt became Moniepoint by pivoting twice, first from bank infrastructure to agent banking, then from business to consumer. PiggyVest added investment products, launched PocketApp as a separate social payments product, and built its own in-house payment infrastructure through PocketApp to replace the virtual account numbers it had relied on since launch. Carbon went from a lender to a neobank over the course of a decade. None of these companies look exactly like their 2016 selves.

It required surviving macroeconomic pressure that would have ended less capitalised companies. The 2023 naira redesign crisis tested every payments company with a liquidity dimension. The naira devaluation that followed squeezed fintech entities with dollar-denominated costs and naira revenues. Moniepoint’s agent network, which kept cash moving during the 2023 cash crunch when ATMs went dark, proved its resilience in the most visible way possible.

What the next decade of fintech has to solve

Ten years in, each of these fintech companies faces a version of the same pressure: how do you grow without replicating the limitations of the institutions you were built to replace?

Moniepoint’s Kenya expansion through Sumac is an early test of whether its Nigeria model travels. Flutterwave’s continental and diaspora ambitions put it in direct contact with regulatory environments that do not move at product velocity. PiggyVest is launching PiggyVest Kids before Children’s Day 2026, moving into a generational dimension of financial behaviour that no Nigerian fintech has successfully owned.

There is also the infrastructure question. The AWS strikes on Gulf data centres in April 2026 exposed a structural dependency that Nigerian fintechs share. All five companies in this cohort run on cloud infrastructure hosted primarily outside Nigeria. Their resilience over the past decade was built on product and operational strength. The next decade will require that same resilience to extend to the physical layer of the internet itself.

A decade ago, the question was whether Nigerian consumers would trust a savings app with their money, whether merchants would route payments through an API instead of a bank counter, and whether an agent with a POS terminal could substitute for a bank branch in a Lagos market.

All five fintech companies answered those questions with numbers. The next set of questions, around sovereignty, scale, and sustainability in a market that is still largely informal and heavily exposed to external shocks, does not yet have answers. What the class of 2015-2016 proved is that Nigerian fintech can build durable institutions. What it has not yet proven is whether those institutions can hold at continental scale.

The post Nigeria’s fintech class of 2015-2016 turns 10 | Here is what a decade built first appeared on Technext.

Ayrıca Şunları da Beğenebilirsiniz

Trump biographer predicts next 3 Cabinet members on the chopping block

Kalshi hires ex-Democratic strategist amid legal troubles