Reserve assets face new test as sanctions risk pushes Bitcoin into policy debate

A recent paper by the Bitcoin Policy Institute on Taiwan opens with a familiar argument that the country's reserves are overconcentrated in dollars. Gold underperforms its potential, and Bitcoin could complement both.

Readers who stop there miss the more consequential claim buried in the blockade-and-invasion framework on pages 5 through 7, where the paper is trying to redefine what makes a reserve asset fail.

Traditional reserve analysis judges assets on liquidity, price stability, and credit quality. The BPI paper adds a fourth test: can the asset still be moved, spent, or mobilized when shipping lanes are blocked, the host state withdraws custodial access, or another state becomes politically hostile?

By that measure, gold can be stranded, dollar reserves can become conditional, and Bitcoin can stay electronically portable regardless of physical access or diplomatic standing.

That is a larger conceptual move than advocating for a Taiwanese BTC position.

Why this matters: This marks a shift from traditional reserve thinking. Assets like Treasuries and gold can remain valuable on paper while becoming difficult or impossible to use under sanctions, conflict, or political pressure. If reserve managers begin prioritizing access over stability, Bitcoin enters the conversation not as a return play, but as a contingency asset.

From macro bet to sovereignty insurance

For years, the state-level Bitcoin argument ran on a single track: hedge monetary debasement, diversify reserves, capture upside from adoption momentum.

That argument still appears in the BPI paper, particularly in its pages on US debt accumulation and the Federal Reserve's balance sheet expansion. The more original contribution sits elsewhere, where the paper ranks reserve assets by whether they stay accessible under coercion.

A government only needs to accept that Treasuries, correspondent banking networks, physically stored metal, and foreign sovereign paper each carry distinct dependencies.

The policy question centers on which asset stays reachable when custody, transport, or host-country politics go wrong.

Official reserve behavior already confirms that framing extends well beyond Bitcoin advocates. The IMF reports that total international reserves, including gold, reached 12.5 trillion SDR at the end of 2024.

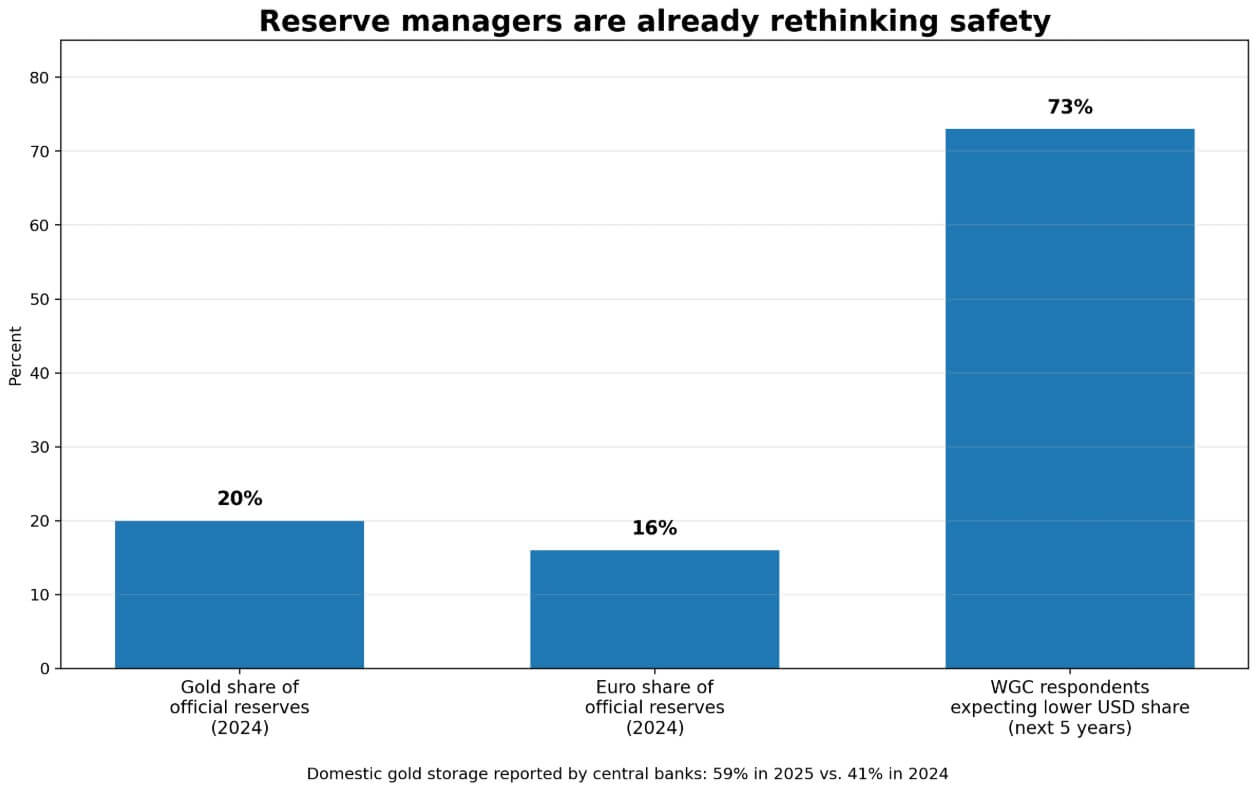

The ECB reported that gold's share of global official reserves reached 20% by market value in 2024, surpassing the euro's 16%, and that central banks bought more than 1,000 tonnes that year.

The World Gold Council's 2025 survey found 73% of respondents expect lower US dollar holdings in global reserves over the next five years, and the share of central banks reporting domestic gold storage jumped to 59% from 41% a year earlier.

Reserve managers are already broadening the definition of reserve risk, and the BPI paper extends that logic to Bitcoin.

| Asset | Normal-times strength | Crisis vulnerability | Failure mode under stress | Why it matters in the article |

|---|---|---|---|---|

| U.S. dollar reserves / Treasuries | Deep liquidity, high credit quality, global reserve standard | Can become politically constrained by host-country policy, sanctions, or custodial leverage | Freeze / conditional access / political pressure | Shows that a reserve can remain “safe” on paper but become less usable in practice |

| Gold | Longstanding reserve ballast, inflation hedge, widely accepted by official institutions | Hard to move quickly, physically trappable, vulnerable to seizure or transport bottlenecks | Stranding / seizure / logistics failure | Explains why portability and physical control now matter more in reserve analysis |

| Bitcoin | Digitally portable, bearer-like, can be moved without shipping lanes or physical transport | High volatility, governance burden, limited official-sector acceptability | Institutional reluctance / policy hesitation, rather than physical immobilization | Enters the story as a potential asset of last-resort accessibility rather than a conventional safe reserve |

| Diversified non-dollar sovereign paper | Reduces reliance on a single reserve issuer, still fits conventional reserve frameworks | Still depends on external sovereign systems, settlement infrastructure, and market access | External dependency / reduced neutrality | Serves as the bear-case alternative: reserve managers may prefer this over BTC even after accepting access risk |

| Domestically vaulted gold | Improves control over custody while preserving gold’s reserve role | Still suffers from transport friction and limited portability in acute crises | Mobility constraint rather than pure custody risk | Shows why gold can benefit from the same access-risk logic without fully solving it |

The live evidence for access risk

The access-risk argument draws force from concrete recent events.

In March, Russia's central bank challenged the EU freeze affecting approximately $300 billion in sovereign funds. That dispute keeps the central premise operational: reserve assets can become politically immobilized while retaining their face value.

An asset owned on paper yet frozen in practice has already failed as a reserve, regardless of its credit rating.

Brazil's central bank drew a parallel conclusion. On Mar. 31, Brazil lifted gold's share of reserves to 7.19% from 3.55% in a single year, while cutting the US dollar share to 72, citing diversification as the driver.

The BPI paper argues Bitcoin belongs in that same diversification calculus, specifically for reserve decisions driven by geopolitical logic.

The US Strategic Bitcoin Reserve adds a distinct data point. The White House order prioritizes the reserve with forfeited BTC, prohibits outright sale, and contemplates additional acquisition only on a budget-neutral basis.

That pulls Bitcoin reserve language into an actual sovereign administrative structure, setting a precedent regardless of its unconventional funding source.

A bar chart shows gold surpassing the euro in official reserves at 20% versus 16%, while 73% of central banks expect to cut dollar holdings within five years.

A bar chart shows gold surpassing the euro in official reserves at 20% versus 16%, while 73% of central banks expect to cut dollar holdings within five years.

Two futures for the sovereign Bitcoin argument

Scale makes the bull case concrete. Taiwan's reserves total roughly $602 billion, and a 1% Bitcoin sleeve would be about $6 billion, while a 5% sleeve would be $30 billion.

The broader math is starker: 0.1% of global reserves, roughly $16.25 billion, would represent about 1.2% of Bitcoin's entire market cap at current prices near $68,000.

Reserve system participation, even at a marginal scale, would have price consequences well before any central bank made a headline allocation decision.

The bull case requires a handful of politically exposed or sanctions-conscious states first to formalize small BTC positions in the 0.25% to 1% range, or to treat already-held seized or mined Bitcoin as a reserve asset before buying more.

Ferranti's sanctions risk modeling supports the direction: in one sanctions scenario, his model produces an optimal Bitcoin share of around 5% for exposed sovereigns. The sovereign Bitcoin discourse would then move from advocacy papers to actual balance sheet entries.

The bear case accepts the access risk critique and still concludes that Bitcoin loses.

Reserve managers acknowledge that physical gold carries logistical dependencies and that dollar reserves carry political ones, and then decide that Bitcoin's volatility, governance burden, and near-zero official-sector acceptability make it a weaker hold than domestically vaulted gold and diversified non-dollar sovereign paper.

Gold absorbs the diversification demand that the access-risk argument was supposed to generate for BTC, and Bitcoin's role as a reserve asset stays conceptual. The debate evolves while portfolios hold their composition.

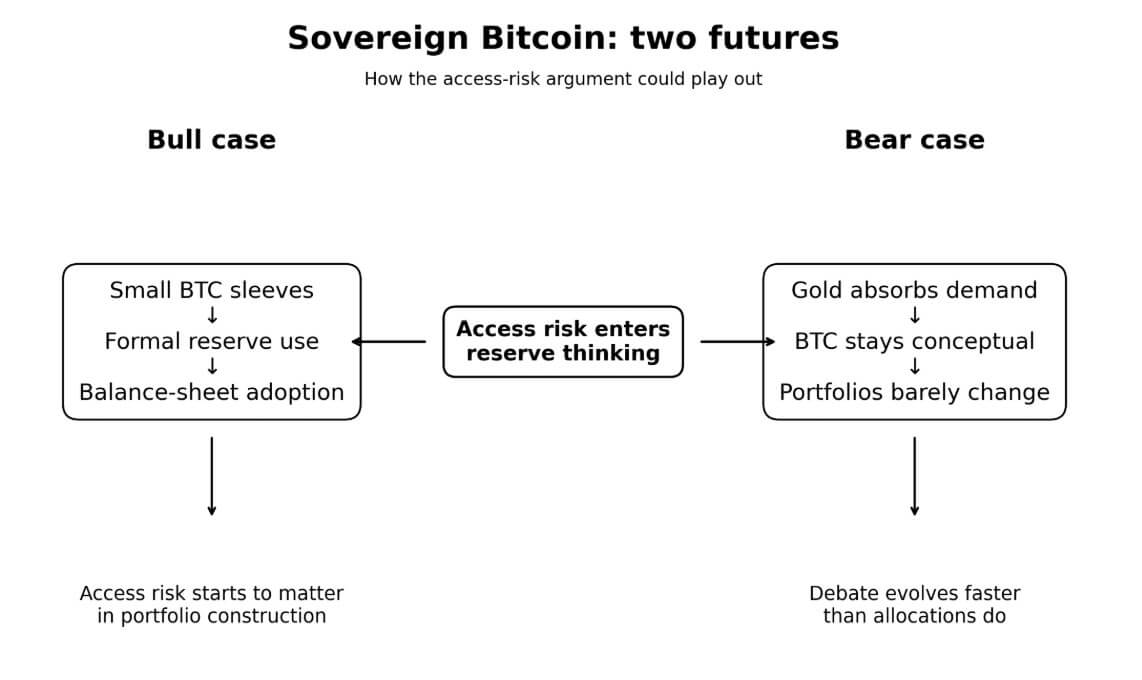

A dual-path flowchart maps how access risk entering sovereign reserve thinking could produce either formal Bitcoin balance-sheet adoption or a debate that outpaces actual portfolio change.

A dual-path flowchart maps how access risk entering sovereign reserve thinking could produce either formal Bitcoin balance-sheet adoption or a debate that outpaces actual portfolio change.

Where the argument holds and where it strains

The BPI paper is strongest when it treats portability and seizure resistance as genuine reserve characteristics, grounded in observable reserve behavior.

That framing tracks official geopolitics now visibly influences reserve composition, and the desire to hold assets outside concentrated single-counterparty dependency is real and already moving portfolios.

The paper overreaches when adoption momentum or price appreciation enters as evidence that the policy case is settled. Official institutions still weigh acceptability, legal clarity, and operational habit alongside access risk, and those factors carry weight that portability rankings leave unaddressed.

The most credible version of the paper's argument is its own stated position: Bitcoin as a small insurance sleeve alongside gold, optimized for access.

For most of Bitcoin's history as a reserve policy topic, the central question in official circles was whether Bitcoin was safe enough to hold. That framing consistently disadvantaged BTC because its volatility kept it below Treasuries and gold on every conventional measure.

Reserve managers are now focused on which assets stay deployable in the event of a hostile geopolitical environment. Gold's resurgence, domestic vaulting preferences, sanctions-driven reserve disputes, and payment-infrastructure fragmentation all show that reserve managers are already seeking conventional assets.

Bitcoin advocates are inserting BTC into that same conversation, and the BPI paper shows how that argument works at its most sophisticated.

The post Reserve assets face new test as sanctions risk pushes Bitcoin into policy debate appeared first on CryptoSlate.

Ayrıca Şunları da Beğenebilirsiniz

Today’s Biggest Crypto Movers: Dogecoin Leads the Pack

RWA Boom Accelerates As Tokenized Assets Hit New Highs In Early 2026