Amgen’s Stock Is Down 10% From Its Highs: The $10 Billion Obesity Drug Bet That Could Define the Next Decade

Key Stats for Amgen:

- 52-Week Range: $269.77 to $391.29

- Current Price: $351.43 (as of June 24, 2026 close)

- Market Cap: ~$190 billion

- Street Mean Target: ~$353

- NTM P/E: 15.5x

- LTM Net Debt/EBITDA: 2.64x

- Dividend Yield: 2.9%

- Q1 2026 Non-GAAP EPS: $5.15 (up 5% year over year)

- Q1 2026 Free Cash Flow: $1.5 billion (up 50% year over year)

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

Amgen Grew Revenue From $26 Billion to $37 Billion in 4 Years. The Estimates Say That Is Just the Beginning

Amgen Inc. (AMGN) has spent the last several years executing one of the more complex transitions in large-cap biotech: absorbing a $28 billion acquisition in Horizon Therapeutics, managing biosimilar erosion in its older blockbusters, and simultaneously building out a new wave of franchises across oncology, rare disease, and inflammation. The revenue chart is the clearest way to see how that transition has gone.

Total revenues grew from $26 billion in 2021 to $36.8 billion in 2025, a climb that absorbed real headwinds along the way. Prolia fell 34% in Q1 2026 as biosimilars launched globally, and Enbrel dropped 37% as Medicare Part D price setting under the Inflation Reduction Act took effect.

These are managed declines that management telegraphed well in advance, and newer franchises are more than covering them.

Amgen Revenue Estimates. (TIKR)

Amgen Revenue Estimates. (TIKR)

What is keeping the revenue line moving is a broad bench of newer products growing at rates older franchises rarely see. UPLIZNA grew 188% year over year in Q1, while IMDELLTRA, a lung cancer treatment, grew 219%.

Repatha, the cholesterol drug, grew 34%. CEO Robert Bradway said on the Q1 call that 16 brands delivered at least double-digit growth. Consensus projects revenue building toward around $38 billion in 2026 and roughly $43 billion by 2030.

See the exact moment Wall Street upgrades a stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

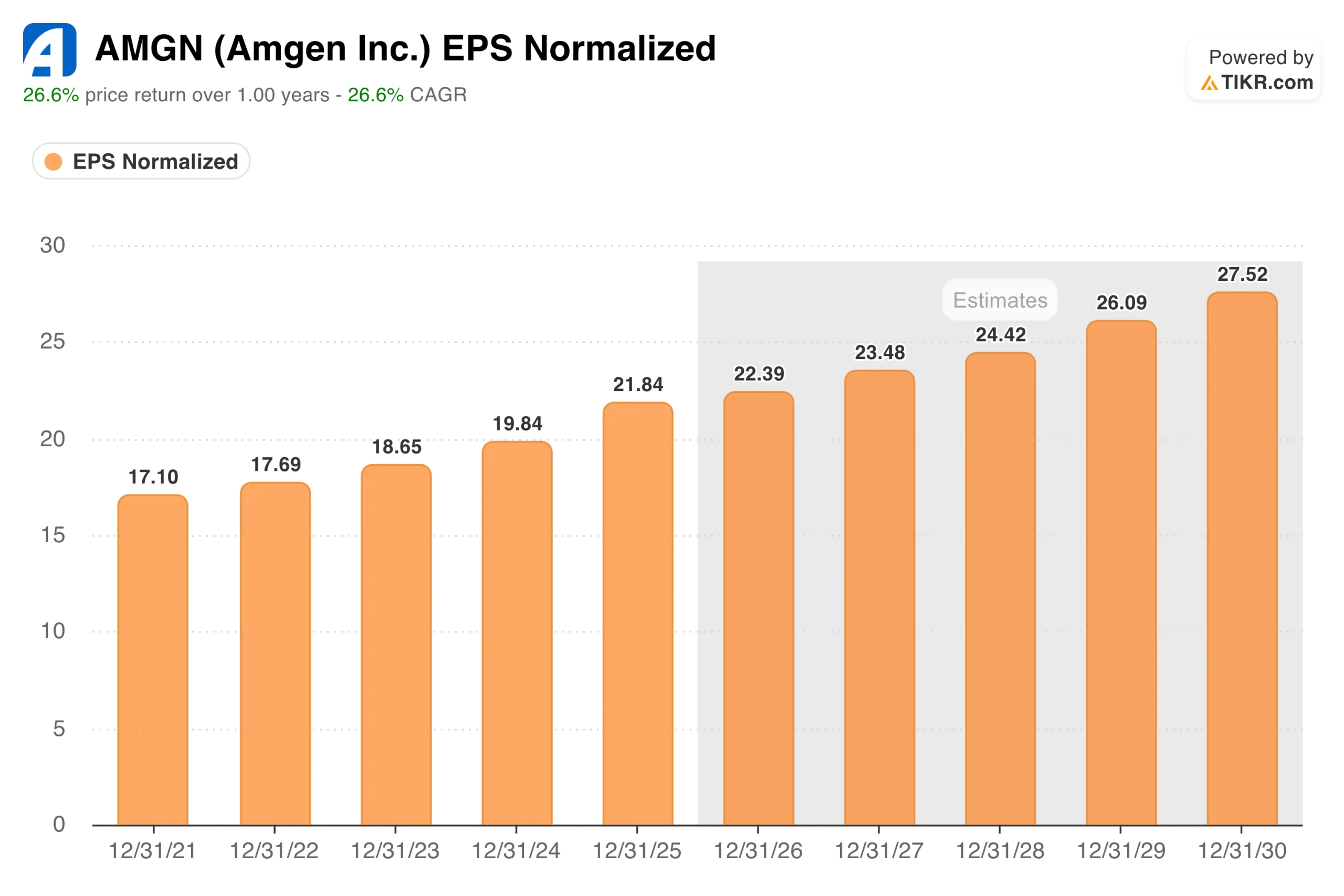

From $17 to $22 in 4 Years: Why Amgen’s Earnings Hold Up Even When the Headlines Don’t

The EPS chart tells the other half of the story. Normalized earnings grew from $17.10 in 2021 to $21.84 in 2025, an uninterrupted climb that spanned the Horizon integration, rising biosimilar headwinds, and a heavier interest burden from the acquisition debt. Q1 2026 non-GAAP EPS came in at $5.15, up 5% year over year and ahead of consensus. Full year 2026 guidance calls for non-GAAP EPS of $21.70 to $23.10.

Amgen EPS Normalized. (TIKR)

Amgen EPS Normalized. (TIKR)

The margin profile underneath those earnings is worth understanding. Non-GAAP operating margin held at 45.3% in Q1, essentially flat year over year, while free cash flow grew 50% to $1.5 billion as amortization on Horizon’s acquired assets begins rolling off.

The business generates substantial cash even when the news cycle is dominated by pipeline updates and regulatory headlines. One item to flag: the FDA proposed in April to withdraw approval of TAVNEOS, a rare-disease drug with annual sales of roughly $500 million.

Amgen has engaged Duke Clinical Research Institute to independently re-evaluate the trial data and plans to contest the decision. It is not thesis-changing, but it is a real overhang investors are watching. Consensus projects EPS approaching around $28 by 2030.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What the TIKR Model Says About Where Amgen Goes From Here

At around 15.5x NTM earnings, Amgen trades at a genuine discount to large-cap biotech peers, and the Street mean target of around $353 sits essentially where the stock trades today. That near-flat implied upside reflects a broadly neutral analyst posture while the market waits for MariTide data. The TIKR mid-case model takes a longer view.

Amgen Valuation Model. (TIKR)

Amgen Valuation Model. (TIKR)

The mid-case targets around $467 per share, implying roughly 33% total return from the current price, or about 6.5% annualized over the next 4.5 years. The model assumes around 3% annual revenue growth and net income margins near 35%, consistent with the historical trajectory and without assigning meaningful credit to MariTide’s success.

The high case reaches around $680. The low case still lands near $485, above today’s trading range.

MariTide is the variable that none of these scenarios can fully capture. It is a monthly or quarterly injection that simultaneously activates the GLP-1 receptor and blocks the GIP receptor, designed to produce durable weight loss with far less frequent dosing than Lilly’s Zepbound or Novo Nordisk’s Wegovy.

Phase 2 showed an average weight loss of up to 20% at 52 weeks, disappointing investors expecting more, and that gap has kept the stock off its highs. Phase 3 data from the MARITIME program are expected through 2027.

Investors buying today are effectively owning a durable, cash-generating biotech at a reasonable multiple, with a meaningful option on one of the most important clinical readouts in the obesity space over the next 18 months.

Should You Invest in Amgen Inc.?

The case for Amgen does not require MariTide’s success. The existing business grows revenue steadily, compounds earnings reliably, and throws off enough cash to support a nearly 3% dividend that has grown at around 12% annually for a decade. At roughly 15.5x forward earnings, that combination is not expensive.

MariTide is the option on top. If Phase 3 data through 2027 show competitive weight loss against weekly GLP-1 drugs, the current price will look like a significant discount in hindsight.

If they disappoint, the core business still justifies owning the stock at levels close to today’s. That asymmetry is what makes Amgen worth a serious look right now.

See the full TIKR model for AMGN, including scenario assumptions and historical valuation multiples. Build your own valuation for Amgen stock on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Polkadot Price History: DOT Hits Sub-$1 in 2026 After $54.87 ATH — What Went Wrong?

She pulled a fast one on MAGA — and paid off her medical debt

NZD/USD Price Forecast: RSI Flashes Oversold as Pair Tests Critical Support Near Seven-Month Lows