Is Domino’s Stock a Buy or a Hold Right Now? Here’s What Analysts Say

Key Takeaways for Domino’s Pizza Stock as of June 2026

- Analysts rate Domino’s Pizza stock 15 Buys, 2 Outperforms, 12 Holds, 1 Underperform, 1 Sell, with a street mean target of $404, implying 29% upside from the current price of $312.

- TIKR’s mid-case model values Domino’s Pizza at $453 by December 2030, implying 45% total return from current levels, or 9% annualized.

- Domino’s Pizza stock has fallen 37% from its 52-week high of $496, yet the street consensus projects EPS recovering to around $4 per quarter through the rest of 2026 before stepping up to around $7 in Q4, a recovery the current price does not yet reflect.

DPZ trades 29% below the street’s mean target. See the full EPS recovery arc and forward estimates on TIKR for free →

Domino’s Pizza Stock Fell 37% While Same-Store Sales Missed but EPS Did Not Collapse

DPZ Stock Q1 2026 Earnings in USD (TIKR)

DPZ Stock Q1 2026 Earnings in USD (TIKR)

Domino’s Pizza (DPZ) has shed 37% from its 52-week high of $496, sitting at $312 as of the June 18, 2026, close, yet Q1 2026 adjusted EPS of $4.13 remained above $4 on a franchise model that grew operating income 6% year over year even as same-store sales disappointed.

Q1 2026 U.S. same-store sales grew 0.9%, well below the company’s 3% target, as consumer confidence fell to COVID-level lows in March and pizza competitors ran promotions directly out of Domino’s own playbook, a deliberate imitation of the value offers the chain has led with for over a decade.

CEO Russell Weiner addressed the competitive moment on the Q1 earnings call: “When competitors match our value, it places significant pressure on their franchisee economics — over time, we expect this pressure to contribute to more store closures on top of the roughly 450 closures our two public pizza competitors have already announced for 2026.”

The international segment added 161 net new stores in Q1 2026, with same-store sales declining 0.4% on a constant-currency basis, driven almost entirely by underperformance at Domino’s Pizza Enterprises (DPE), the brand’s largest global master franchisee managing markets across Australia and several other regions, and CFO Sandeep Reddy noted that excluding DPE, the international business performed in line with expectations.

Management revised full-year U.S. same-store sales guidance to positive low single digits from the prior 3% target but held its unit growth outlook, committing to 175-plus net new U.S. stores and roughly 800 internationally, a signal that the franchise pipeline remains strong even as near-term comps underwhelmed.

Through April 21, Domino’s repurchased approximately 446,000 shares for $170 million year-to-date, and the Board added a new $1 billion repurchase authorization on top of the prior remaining balance, leaving $1.29 billion in total buyback capacity, a figure that reflects management’s conviction in the long-term earnings trajectory regardless of the near-term macro.

Track DPZ’s quarterly EPS against the forward consensus and see whether the $404 mean analyst target holds through Q2. Pull up the estimates table on TIKR for free →

Wall Street Is Split on Whether DPZ’s 2026 Pressure Is Transitory or a Structural Reset

Street Analysts Target for DPZ Stock (TIKR)

Street Analysts Target for DPZ Stock (TIKR)

Domino’s stock carries 15 Buy ratings, 2 Outperforms, 12 Holds, 1 Underperform, and 1 Sell as of June 18, 2026, with a street mean target of $404, implying 29% upside from $312, and a street high of $544, which would represent 74% upside.

DPZ Stock EPS and Revenue Actuals & Estimates (TIKR)

DPZ Stock EPS and Revenue Actuals & Estimates (TIKR)

Q1 2026 adjusted EPS of $4.13 missed the street estimate of $4.27 by 3% and fell 5% year over year from $4.33, but the miss traced directly to the same-store sales shortfall rather than any structural breakdown in the franchise model’s unit economics.

The forward consensus projects a materially different trajectory than the current price implies, with analysts estimating Q2 2026 EPS of around $4, Q3 EPS of around $4, and a Q4 step-up to around $7, the sequential acceleration driven by the 53rd-week comparison period and management’s planned second-half product launches and updated marketing calendar.

Domino’s Pizza stock’s Q1 revenue of $1.15 billion grew 3% year over year versus the street’s $1.16 billion estimate, a near-miss of less than 1%, not the kind of top-line structural break that would justify the stock trading at a 37% discount to its 52-week high.

The analyst price target cuts concentrated in late April reflect a reset to a lower comp assumption for the full year, not a thesis inversion. Thirteen firms lowered targets while retaining Buy or equivalent ratings, with only two firms holding below-consensus positions, suggesting the majority of the Street treats the current price as a buyable reset rather than a structural failure.

Berkshire Hathaway’s full exit of its DPZ stake in Q1 2026 dominates sentiment headlines, but that portfolio decision followed the leadership transition from Warren Buffett to Greg Abel and reflected a broader portfolio reshuffling across dozens of positions rather than a thesis-specific call on Domino’s franchise economics.

Domino’s Pizza stock’s Q2 2026 earnings call on July 20 is the first concrete test of whether the macro headwind is softening, and U.S. same-store sales in the 2%-to-3% range would give the Hold camp no remaining reason to stay on the sideline.

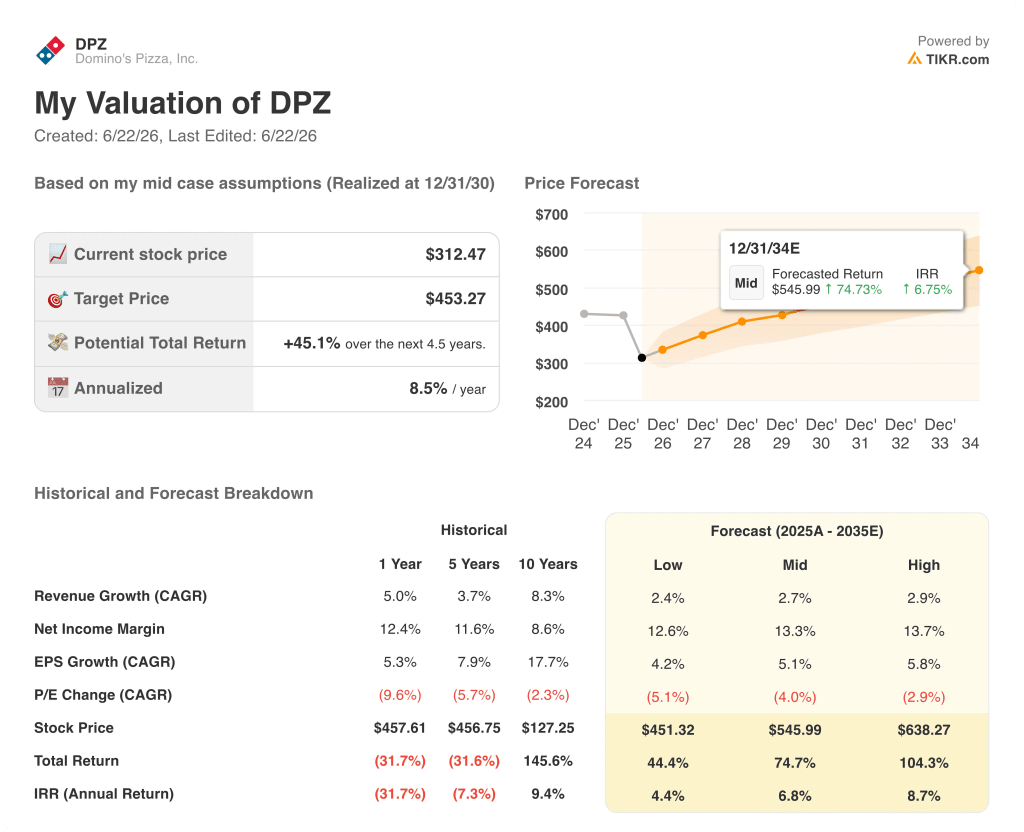

Is Domino’s Pizza Stock Undervalued in 2026? TIKR’s $453 Mid-Case Says Yes

TIKR’s mid-case model values Domino’s Pizza at $453 by December 2030, implying 45% total return from the current price of $312, or 9% annualized over 4.5 years.

DPZ Stock Valuation Model Results (TIKR)

DPZ Stock Valuation Model Results (TIKR)

The model’s mid-case assumes revenue growing at a 3% compound annual rate through 2035 and net income margins expanding to 13%, consistent with the franchise-and-supply-chain structure that already generated 19% operating margins in Q1 2026 on one of the weakest same-store sales quarters the business has posted in years.

The franchise system’s profit trajectory supports those assumptions. Average franchisee profits rose roughly $80,000 per store over the past 11 years, and the $1.29 billion buyback authorization provides a mechanical tailwind to EPS growth that runs independently of any single quarter’s comp performance.

At $312, Domino’s Pizza stock prices in permanent macro damage, yet the TIKR model requires only a continuation of the low-single-digit revenue growth and margin stability the business has already demonstrated across eight consecutive quarters to reach $453.

Explore the full TIKR model for DPZ and stress-test the same-store sales assumptions against the Q2 comp data dropping July 20. Build your DPZ model on TIKR for free →

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Domino’s Pizza, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Domino’s Pizza, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DPZ stock on TIKR for Free →

You May Also Like

Google Searches Could Expose Users to Crypto Wallet Risks

Morgan Stanley Revises Ethereum and Solana ETF Filings to Unveil Record-Low Fees

LIST: Bayanihan initiatives amid soaring oil prices

Trending News

More24/7 Live News

MoreQuick Reads

More