How NectarFi’s Stephanie Okeke is building the infrastructure layer that crypto forgot

Most people do not think about the pipes that move water through their homes. They just turn on the tap. This is how Stephanie Okeke thinks about fintech. Not the app, not the interface, not the gloss of it.

The invisible layer underneath that has to work so flawlessly that users never have to know it exists. It is the opposite of how most founders talk about what they are building, and it is why NectarFi, the crypto startup she co-founded with Felix Daniel, might actually matter.

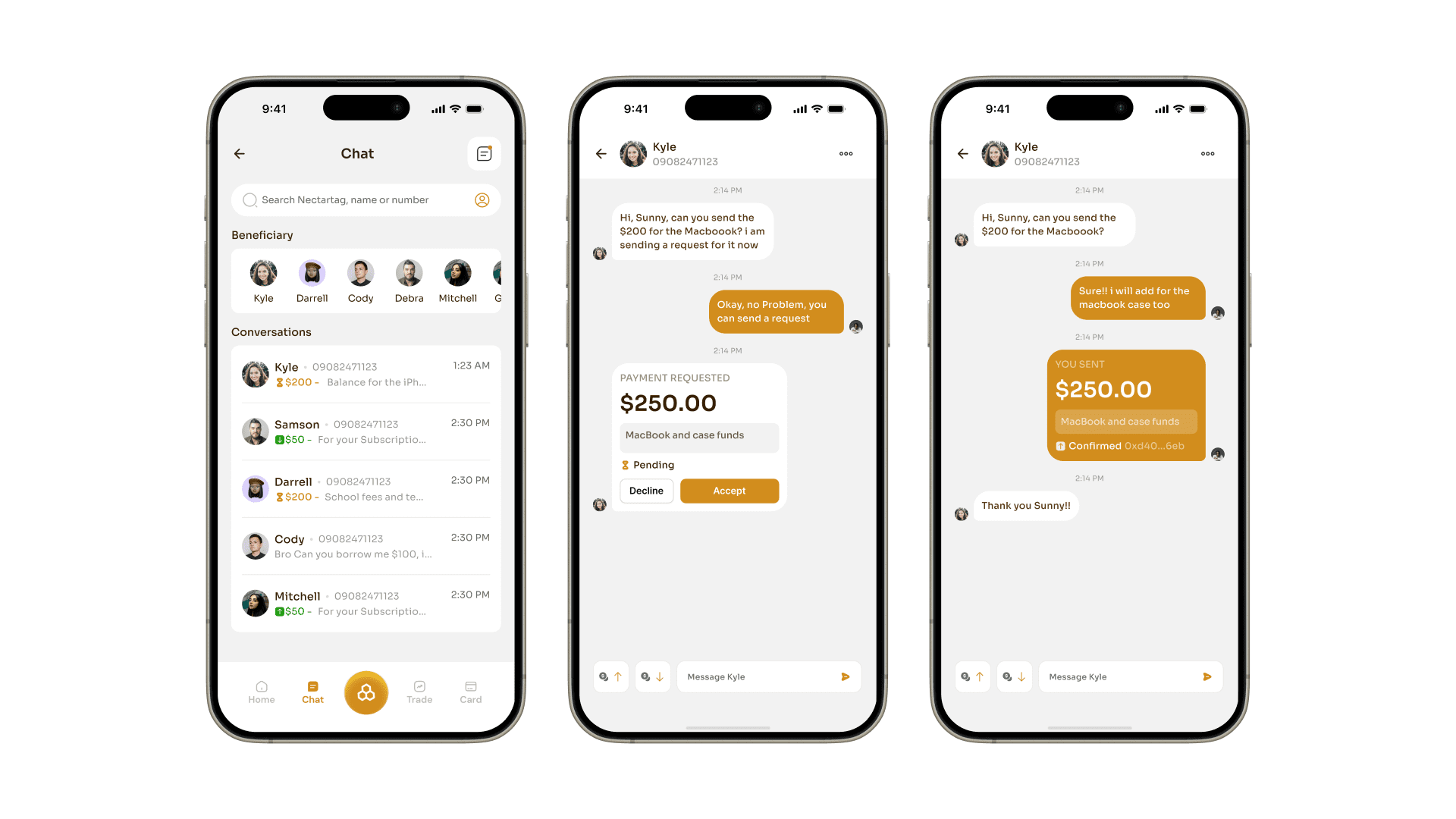

When you open NectarFi, what you see is simple. You have naira and want to invest. You tap a button. One minute later, you own a token in your own wallet. Done. One flat fee, and no confusion.

What you do not see is everything that had to break itself in half to make that simplicity real.

“On a typical wallet or exchange, a first trade is a five-step ordeal,” Okeke explains. “Find a P2P seller for USDC, move it across, swap to SOL for gas, then finally swap into the token you actually wanted, paying gas twice and a heavy fee, 45 minutes gone. On NectarFi, naira deposits, converts to USDC, tap the token slash invest slash save, done, about a minute, one flat fee.”

Stephanie Okeke, co-founder, Nectarfi

Stephanie Okeke, co-founder, Nectarfi

That one minute is worth unpacking. It means NectarFi built its own naira on-ramp, so there are no P2P middlemen bleeding margins. It means they aggregate Solana liquidity across exchanges to find the best price every time. It means they absorb the network gas fees themselves, so users never wake up to surprise charges when the blockchain gets congested. They take that cost onto their own books. They eat it, so a user in Lagos or Nairobi sees one number and pays it.

This is what infrastructure first actually looks like.

But the larger bet is that Okeke built all of this while ensuring users keep complete control of their money.

The keys stay on the user’s device. Always. Your keys, your funds, your sovereignty. That is the opposite choice from what most exchanges make. Custody would be easier. Custody would be more profitable. Custody would open the float, the investment income, the fees that make crypto exchanges rich.

Okeke chose the harder path.

“That is the line we will not cross, even though holding funds would be easier to build and would open up the custodial revenue an exchange makes,” she says. “The trade-off is more work, more cost, and a harder regulatory job for us, so that the user just sees their naira become a token they own.”

This is a choice. And it reveals something about how Okeke thinks: infrastructure that serves the user means sometimes you have to take the cost yourself. Sometimes you have to build the hard thing underneath so nobody has to think about it.

Nectarfi app

Nectarfi app

Solving the “Last Mile” problem in African fintech

She did not start out thinking this way. When NectarFi began, she thought they were building a consumer product. The standard crypto startup story: beautiful interface, go viral, scale. Six months in, reality hit.

“We realised the product was the easy part,” Okeke says. “The rails underneath were where everything either worked or died. In the Global South the last mile is broken: the off-ramps, the credit history, the trust. That is not a feature you bolt on, it is the whole game.”

This is the insight that changed her. The last mile is the entire problem. A crypto earner in Nairobi might be making real money, but that money exists in a blockchain ledger. The moment it has to become rent, become food, become naira, the system breaks. And worse, that person remains completely invisible to credit. No score. No history. No way in.

So Okeke decided to build what nobody else in crypto is even thinking about: a credit layer.

Building a blockchain-based credit identity layer

“Crypto thinks about transactions,” she says. “We are building the credit identity underneath. A freelancer in Lagos or a crypto earner in Nairobi can be making real money on chain and still be completely invisible to credit, no score, no history, no way in. We are building a credit score from how people actually earn and save on NectarFi, so the rail does not just move their money, it lets the system finally see them.”

This is where the infrastructure philosophy becomes something larger. The pipes are not just moving money faster. The pipes are building financial identity for people that the formal system has never seen. Every transaction, every save, every repayment is data. Data that compounds over time. Data that becomes a credit score for people who have never had one.

And yes, this creates a moat. But it is not the kind of moat that other fintech companies can copy in a month.

“Anyone can clone a clean interface in a month,” Okeke says. “Nobody clones a working naira off-ramp or a credit score built on months of behavioural data. Trading is the wedge, it is why people show up. The infrastructure underneath, and the credit layer especially, is why they cannot leave.”

Why patience and data collection are NectarFi’s ultimate moat

The trade-off for this vision is patience. Nectarfi raised $200,000. $170,000 of it got them live. That is not much runway when your moat only gets stronger with time and volume.

“A behavioural credit score only sharpens as real repayment data accumulates across thousands of users over many months,” she explains. “That compounding is the moat, and it is exactly the part you cannot buy or rush. What keeps me up at night is the asymmetry: our deepest moat is also our slowest to compound, and runway is what buys the time to let it mature.”

This is honest in a way that founder interviews rarely are. Most would talk about growth, momentum, and network effects. Okeke talks about what terrifies her: the gap between what her business needs (data, time, users) and what her funding allows (speed, depth, patience).

She says no to things other founders would say yes to. She could ship aggressive lending tomorrow. Her users are desperate for credit, and she has the data to offer it. But she does not.

Stephanie Okeke, co-founder, Nectarfi

Stephanie Okeke, co-founder, Nectarfi

“We could ship aggressive lending tomorrow, everyone wants credit, and our users are underserved and eager for it,” she says. “But extending credit fast and loose to people the formal system has never scored is exactly how you build a beautiful default crater. So we are deliberately patient: we watch real behaviour before we offer anyone a line, we start conservative and let limits earn their way up.”

This patience is hard-won conviction. It comes from understanding that you cannot build trust quickly. You can only build it honestly, and that takes time.

There is something else nobody outside the company knows yet. Something that will matter more in two years than anything else she is building right now.

"NectarFi is actually more of a data company than a fintech product," Okeke says. "We built a credit algorithm in-house that builds portable credit profiles for our users, and this will soon be the bedrock for FIs and other credit companies. Every save, every trade, every on-time peer payment is data we are collecting now, long before the credit score is even a public product. It earns us nothing today. In two years, it is the moat, because behavioural scoring for people with no bureau record is something you can only have if you started collecting honestly and early."

This is the real bet. Not the app. Not the Solana integration. The quiet work of building a credit system from the ground up for people the world has never counted.

The pipes. The invisible things that have to work so users never have to think about them. Stephanie Okeke is building those pipes. And she is betting her company that nobody else will.

Read also: From getting a 4/20 in French, Owoade Apotierioluwa built a multilingual AI to help others

You May Also Like

Polymarket Paid Creators To Film Fake Trades In Covert Social Media Campaign, Investigation Finds

Current price of oil as of June 22, 2026

Ares Strategic Mining Establishes New Investor Relations Team Following $10 Million Funding