Why the CBN wants to know who really owns Nigeria’s fintech firms and banks

The Central Bank of Nigeria’s (CBN) June 15 circular asking banks and payment firms to disclose their ultimate beneficial owners reads, on its face, like routine housekeeping. Read against the last three years of regulatory activity around Nigeria’s financial system, it looks closer to a closing of loops the CBN has been tightening since the country exited the Financial Action Task Force (FATF) grey list.

The directive requires all deposit money banks, payment service providers, and other financial institutions with digital payment footprints to disclose the ultimate beneficial ownership of significant shareholders, in line with existing anti-money laundering, counter-terrorism financing, and counter-proliferation financing regulations.

There is no public registry contemplated in the circular itself, only a duty to disclose upon request, which keeps the information within supervisory reach rather than in the open.

Nigeria spent close to two years under FATF’s increased monitoring before being removed from the grey list in October 2025, a process that hinged substantially on demonstrating stronger beneficial ownership transparency and improved prosecution of money laundering cases. Exiting the list did not relax the underlying expectations. If anything, the CBN has spent the period since reinforcing them, including a March 2026 circular ordering banks and other regulated institutions to deploy automated transaction monitoring systems within 18 to 24 months, with implementation roadmaps due by June 10, 2026, just days before this latest mandate.

The beneficial ownership requirement sits naturally alongside that earlier directive:

- February 2023: Nigeria is placed on the FATF grey list, triggering intense regulatory scrutiny.

- October 2025: Nigeria officially exits the grey list after upgrading its transparency frameworks.

- March 2026: The CBN mandates automated AML transaction monitoring solutions.

- June 2026: The CBN ties ownership data directly to market share limits.

Automated systems can flag a suspicious transaction in real time, but they cannot answer who ultimately controls the entity moving the money if that information sits buried behind layered shareholding structures, nominee arrangements, or offshore holding companies.

Piercing the corporate veil to enforce CBN market caps

That gap matters more in Nigeria’s payments sector than the circular’s brief explanatory language lets on. The CBN’s own framing cites concerns about market concentration and the emergence of operators with substantial market presence across key payment activities, language that echoes long-running questions about ownership concentration across Nigerian banking more broadly, where a small number of individuals and family-linked entities have built significant stakes across multiple institutions over the past two decades.

Whether or not the CBN had specific cases in mind when drafting the June circular, the structural condition it describes (opaque ownership sitting underneath rapid market growth) is one regulators have flagged repeatedly in submissions to FATF-style mutual evaluations and in domestic banking sector reviews.

The timing also lines up with the market structure rules introduced in the same circular, which cap any single institution’s share of card issuing or merchant acquiring activities at 25%, with a corresponding 15% ceiling in the alternative activity once that threshold is crossed.

| Activity Segment | Base Market Share Cap | Cross-Market Cap (If Base Exceeded) |

| Card / Consumer Issuing | 25% | 15% (in Merchant Acquiring) |

| Merchant Acquiring | 25% | 15% (in Card Issuing) |

Enforcing a market share cap requires knowing, with confidence, which entities are related and which are genuinely independent. A holding company structured to appear as several unconnected operators could otherwise stay under the radar of a market share calculation that only counts what is visible on paper. Beneficial ownership disclosure closes that particular avenue, at least on paper, by requiring institutions to look through their own shareholding layers and report what they find.

None of this means the disclosure requirement will be straightforward to enforce. The CBN’s mechanism for verification, beyond requesting records and threatening supervisory sanctions for noncompliance, is not detailed in the circular, and Nigeria’s broader corporate registry infrastructure has historically struggled to keep beneficial ownership data current even where disclosure is technically mandated.

The Corporate Affairs Commission (CAC) has maintained a beneficial ownership register since 2021 under the Companies and Allied Matters Act, with mixed results on data quality. Whether the CBN’s payments-specific version improves on that record will depend on how aggressively the bank pursues verification rather than simply collecting attestations.

What the circular does signal clearly is that the CBN no longer treats ownership opacity and market concentration as separate problems. The pairing of beneficial ownership disclosure with hard market share limits in a single directive suggests the bank sees the two as mutually reinforcing risks, where hidden ownership is precisely the mechanism by which concentration limits could otherwise be circumvented.

You May Also Like

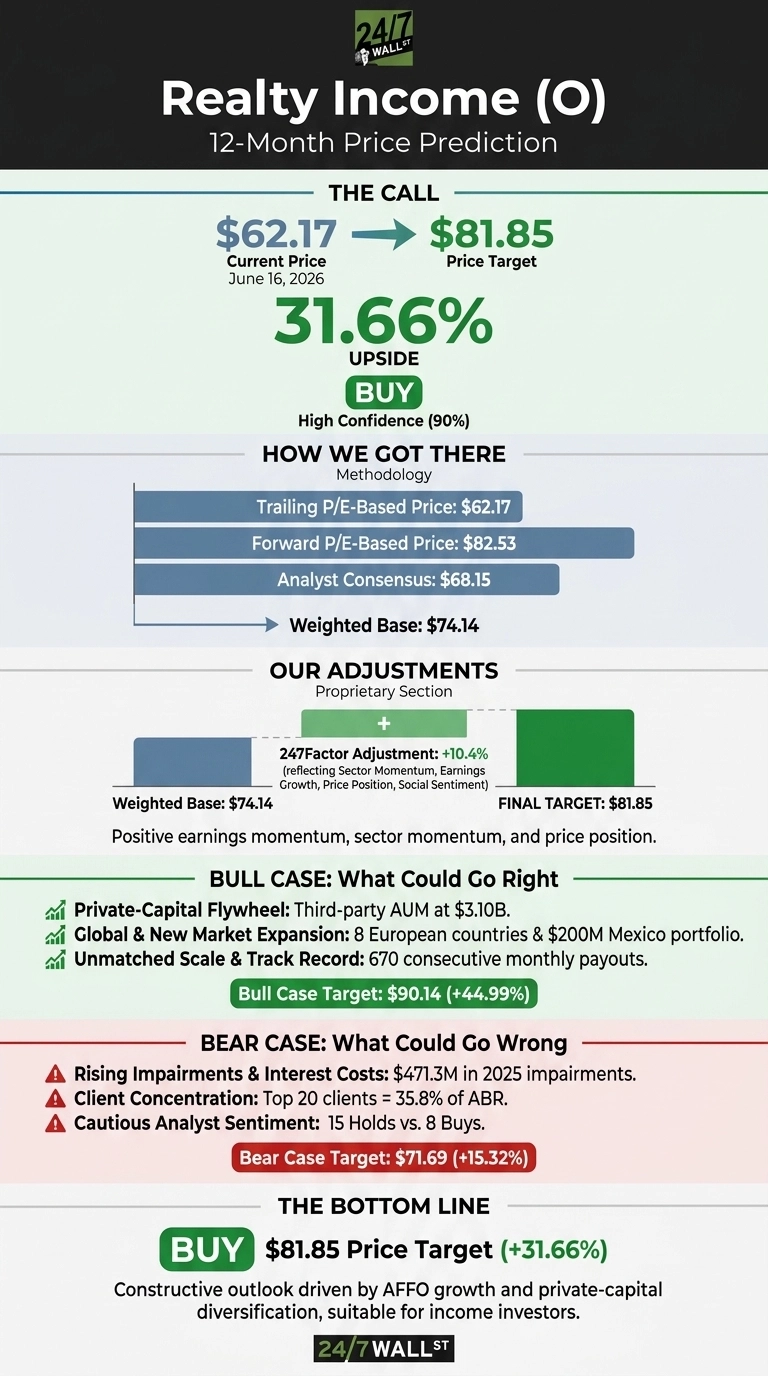

Our Highest Conviction Call on Realty Income Points to 30% Upside

Critical USDT0 Response to Drift Hack Exposes Stark Contrast in Stablecoin Security Protocols

Richard Harris Law Firm Partners with CCSD to Honor School Bus Drivers at Appreciation Event