DeFi’s Potential: Insights for Long-Term Crypto Investors

Decentralized finance is reshaping how investors approach long-term cryptocurrency strategies, from smart-contract liquidity and tokenized real-world assets to AI-powered financial systems. Industry experts have identified thirteen critical areas where DeFi offers practical advantages for patient capital allocation. This article breaks down each opportunity with professional insights to help investors make informed decisions about the future of programmable money.

- Back Real-World Asset Tokenization

- Deploy AI Financial Agent Systems

- Accelerate B2B Settlement With Blockchains

- Adopt Shared On-Chain Records

- Enable Composable Wallet Reputation

- Choose Yield-Bearing Spendable Stablecoins

- Seek Durable Usage-Backed Returns

- Pursue Code-Governed Credit

- Favor Utility-Driven DeFi Ecosystems

- Build Bot-Resistant Market Intelligence

- Leverage Restaked Pooled Security

- Embrace Smart-Contract Liquidity And Escrow

- Prioritize Transparent Verifiable Protocols

Back Real-World Asset Tokenization

Among the various developments in DeFi, the tokenization of real-world assets stands out as one of the most promising for long-term investors. For years, DeFi was largely confined to crypto-native assets. We are now seeing treasury bills, bonds, credit products, and other traditional financial instruments move on-chain.

This matters because it connects blockchain infrastructure with real economic activity. Investors can potentially access yield-generating assets in a more transparent and efficient way, while institutions gain access to programmable settlement and global liquidity.

The long-term opportunity is not about replacing traditional finance overnight. It is about making financial products more accessible, transparent, and interoperable. If this trend continues, DeFi could gradually become part of the underlying infrastructure that powers global financial markets.

“The most important phase of DeFi will begin when it starts bringing real-world assets on-chain, not when it creates another crypto-native product.”

The future of DeFi is likely to be measured less by speculation and more by how much real economic value it can bring onto blockchain networks.

Deploy AI Financial Agent Systems

One DeFi development I believe holds major long-term promise is the rise of AI-assisted automated trading and yield-management bots.

The bigger idea is not simply “bots that trade crypto.” It is that every person could eventually have a personal financial agent that monitors markets, manages risk, allocates capital across DeFi protocols, and looks for income opportunities around the clock. Today, early versions of this are already possible: automated systems can rebalance portfolios, identify arbitrage or yield opportunities, execute strategies, and help users participate in DeFi without needing to sit in front of charts all day.

I believe this could become one of the most important paths toward broader financial independence. Imagine a future where people do not rely only on wages, savings accounts, or traditional wealth managers, but also have their own AI-powered finance assistant working daily to generate yield, manage exposure, and compound returns. That does not mean risk disappears. DeFi still has smart contract risk, volatility, liquidity risk, scams, and strategy failures. But the promise is powerful: finance becomes programmable, personalized, and accessible to far more people.

DeFi could reshape the financial landscape by removing many of the old gatekeepers. Instead of needing a bank, broker, or fund manager to access sophisticated financial tools, individuals could interact directly with open protocols and intelligent automation. Over time, I think the combination of DeFi plus AI agents could turn personal finance from something passive and institution-controlled into something active, global, and user-owned.

That is the future I write about every day: a world where people can use AI and decentralized finance not just to speculate, but to build daily income systems and take more control over their financial lives.

Accelerate B2B Settlement With Blockchains

Quick framing. I am not a DeFi specialist or crypto-native investor. I am Dane Maxwell, founder of Paperless Pipeline, a SaaS bootstrapped on cash flow since 2009. As a founder with a long-horizon view on capital allocation, I do hold a position in the long-term crypto thesis and have watched the DeFi space for years. Happy to contribute the bootstrapped-founder perspective on what is and is not interesting in DeFi.

The DeFi development I believe holds the most significant long-term promise. On-chain settlement of real-world business payments, specifically B2B accounts-receivable cycles.

Why this is the answer. The most expensive friction inside any small business I have run is the gap between invoice issued and cash received. Across our 1,700+ brokerage customer base, the average commission disbursement timeline is 5 to 7 business days from contract close. That gap costs the small business owner cash flow flexibility, lost interest, and operational stress. The traditional banking rails make the gap inevitable because of intermediate verification steps.

The on-chain version of the same transaction settles in minutes, not days, with the verification logic embedded in the smart contract rather than in the back office of three intermediary institutions. For a small business with $5M to $20M in annual receivables, the difference between 5 day settlement and 5 minute settlement is roughly 7 to 12 days of working capital freed up year-round. That is real money for a real business.

The honest caveats. The current DeFi tooling is not built for non-crypto-native small business owners. The user experience assumes a comfort with wallets, gas fees, and protocol risk that the typical brokerage owner does not have. The financial gain is real; the adoption barrier is also real.

The bet for long-term investors. The protocols and infrastructure layers that make on-chain business payments invisible to the end user (the equivalent of how Stripe made online payments invisible in the 2010s) will be the disproportionate winners over the next decade. Crypto-native consumer applications will remain a smaller market than crypto-native business infrastructure.

Adopt Shared On-Chain Records

One development I believe holds significant promise for long-term crypto investors is Web3’s ability to create distributed, single sources of truth for client data and digital assets. At NextGen Wealth we standardized work into our COLLAB financial planning process and moved calculations into a shared, client-facing tool, which showed me how visible records reduce rework and errors.

Applied to DeFi, the same approach could make ownership and transaction histories more visible and verifiable across wallets, custodians, and platforms. That visibility may help long-term investors track holdings, validate fees, and reduce mismatches that currently require manual reconciliation. It also empowers clients to engage directly with transparent records while allowing advisors to focus more on strategic advice than clerical tasks.

Over time, clearer records and lower reconciliation costs could increase trust in crypto infrastructure and make it easier to integrate DeFi into broader financial planning.

Enable Composable Wallet Reputation

Composable Reputation Layers Unlocked Cross-Protocol Borrowing

I’m Ankush Gupta, founder of a Web3 media and PR business that has worked with DeFi protocols since 2020.

The most undervalued development in DeFi right now is on-chain reputation systems tied to wallet history. Not credit scores imported from traditional finance. Native blockchain reputation that tracks transaction patterns, protocol interactions, and long-term behavior across chains.

Here’s why this matters from a PR and visibility lens. We worked with a DeFi lending protocol last year that was exploring reputation-based lending tiers. The team had built a scoring model that assigned trust levels based on how long a wallet had existed, what protocols it had used, whether it had repaid previous loans, and how it behaved during volatility. Wallets with higher scores could borrow at better rates without over-collateralizing.

The insight we had while building content around this: reputation is the missing primitive that makes DeFi accessible to people who don’t have capital to lock up. Traditional finance runs on credit history. DeFi has been running on collateral ratios because there was no other trust mechanism. On-chain reputation changes that.

For long-term investors, protocols that build composable reputation layers have structural moat potential. If your wallet reputation can move across protocols the way your credit score moves across banks, that creates network effects. You behave well on one platform, it benefits you on ten others. Protocols that adopt shared reputation standards early will likely capture more users and liquidity over time.

From a financial infrastructure perspective, this is how DeFi stops being a playground for capital-rich participants and starts functioning as actual alternative finance. Reputation allows unsecured lending. Unsecured lending allows people without existing crypto holdings to participate. That’s when adoption moves from speculative to structural.

The challenge right now is fragmentation. Most reputation systems are protocol-specific. Once interoperability improves and a few credible standards emerge, this becomes foundational infrastructure, not a feature.

Choose Yield-Bearing Spendable Stablecoins

Caveat: I’m a UK marketing-agency founder rather than a DeFi developer, but I hold a personal crypto position and track DeFi developments because several clients sit adjacent to the space. The DeFi development I’d flag as holding significant long-term promise:

The development: programmable yield-bearing stablecoins integrated directly with traditional payment rails.

The mechanic: Traditional stablecoins (USDC, USDT) hold a peg to fiat but don’t generate yield for the holder — the yield is captured by the issuer through treasury-bill returns. Yield-bearing stablecoins like sDAI, Ondo’s USDY, and newer entrants pass that treasury yield through to holders. The result: a holding that maintains fiat-peg stability while accruing roughly current treasury rates (4-5% annually in the recent environment).

Why this matters for adoption: Consumer adoption of DeFi has been blocked by the cognitive load of yield generation. Earning yield required understanding lending protocols, liquidity pools, smart-contract risk, and gas mechanics. Yield-bearing stablecoins remove all of that — the yield is baked into the holding itself, no user action required. The mental model becomes “holding stablecoin that automatically earns interest” rather than “complex DeFi participation.”

The integration with payment rails: The combination that’s emerging in 2026 is yield-bearing stablecoins held within consumer-facing wallets that integrate with traditional card rails. The user holds USDY or similar, the wallet supports tap-to-pay or card transactions, and the user earns yield on idle balance while retaining instant spending access. This collapses the trade-off between earning yield (locked) and spending access (idle) that has historically defined consumer banking.

The implications: If the integration matures, consumer banking faces structural pressure. Why hold cash in a checking account at 0.01% when a yield-bearing stablecoin wallet pays 4-5% with equivalent spending utility? The incumbent bank’s economic model depends on the answer being “regulation, trust, familiarity” — and all three of those answers weaken over time.

The single principle: The most important DeFi developments aren’t the most technically novel. They’re the ones that collapse the cognitive load required to access existing DeFi benefits. Yield-bearing stablecoins do that for the largest stablecoin use case.

Seek Durable Usage-Backed Returns

The DeFi shift that matters most is boring on the surface, stable on chain yield that comes from real usage, not token hype. Long term investors don’t need another flashy protocol. They need something that works under pressure, every day, with tight margins and no room for mistakes.

I look at DeFi the way I run turnover cleaning. We live inside a hard four hour window, 11 a.m. checkout to 3 p.m. check in. If a process can’t hold up there, it isn’t real. Same with DeFi. If a yield source only works in perfect conditions, I don’t trust it.

The promising development is infrastructure that can keep producing predictable returns from actual demand, lending, payments, trading, settlement, without depending on constant price appreciation.

In my business, we cap each cleaner at three properties a day. Push past that and our photo defect rate doubles. That’s a simple lesson in system design. Capacity matters. Reliability matters more than squeezing out one more unit of output.

DeFi has the same fork in the road. The protocols with the best long term future are the ones built for risk controls, transparency, and sustainable throughput, not the ones dangling the highest temporary yield. If DeFi gets that right, it can reshape finance by making core services programmable, visible, and open around the clock. Savings, credit, and income won’t be gated by bank hours or geography.

My rule is simple, if the return depends on hype, it won’t last. If it survives real operational stress, that’s where long term capital belongs.

Pursue Code-Governed Credit

I don’t really follow most of DeFi anymore the way people online expect you to. Too much of it is recycled speculation with new labels. My background in cybersecurity makes me default to distrust systems that move money without clear accountability, and a lot of DeFi still sits in that uncomfortable zone.

The one development I keep coming back to is on-chain lending and automated credit systems. Not the hype layer around it, but the basic idea that lending rules, collateral checks, and repayment logic are executed by smart contracts instead of being manually controlled inside banks or layered intermediaries.

Collateral is visible on-chain. Liquidation rules are visible. In simple cases, you don’t need half a banking stack in the middle deciding outcomes. Interest rates move based on supply and demand inside the protocol, not policy decisions sitting far away from the actual flow of capital. From an automation point of view, this is just replacing manual financial logic with code that executes consistently. Nothing magical, just less human discretion in a narrow slice of finance.

For long-term investors, the real signal is not token price movement. It’s whether capital usage is transparent and continuously verifiable. In traditional finance you wait for reports. Here, you can see how money is actually deployed in real time. Risk doesn’t disappear, but it becomes more observable, which already changes behavior.

I don’t think DeFi replaces banking wholesale. That claim is mostly noise. But repetitive parts like basic lending, settlement, and asset transfer are already being pulled into code-based systems. Banks still matter for identity, regulation, and large-scale trust problems. What shifts first are the mechanical workflows.

From building automation systems, I’ve seen this pattern before. Tools don’t replace entire industries at once, they quietly remove repeatable steps until cost structures change.

If I had to give one practical filter: ignore narratives and watch usage. Real lending volume that survives quiet markets tells more than any hype cycle. Most projects look strong until activity is tested over time. That’s usually where the real answer shows up.

Favor Utility-Driven DeFi Ecosystems

One of the more interesting developments in decentralized finance is the emergence of ecosystem-backed financial platforms that focus on sustainability and real-world utility instead of pure speculation. A project I’ve been watching closely is [Reaper Financial](https://www.reaper.financial/) and its token, Reaper (RPR).

What makes projects like Reaper stand out is that they are trying to bridge the gap between decentralized finance and practical economic infrastructure. Too much of DeFi’s first generation revolved around unsustainable yield farming, meme speculation, and token velocity without underlying value creation. Long term investors should be paying attention to projects that are building actual ecosystems with payments, governance, utility, and community alignment at the center.

The larger promise of DeFi is not simply replacing banks. It is rebuilding financial coordination from the ground up with transparent, programmable systems. Smart contracts can automate lending, settlement, insurance, escrow, and asset transfers without requiring layers of intermediaries. That reduces friction, lowers transaction costs, and potentially opens financial access to people and businesses that traditional systems ignore.

For investors, the long-term opportunity is in platforms that create durable network effects. If a DeFi ecosystem can support commerce, governance, treasury management, and cross-border transactions while remaining decentralized and secure, it starts to resemble digital infrastructure rather than a speculative token project.

The financial landscape could change substantially over the next decade because DeFi introduces a model where individuals control assets directly, transactions settle globally in minutes, and financial products become open-source and composable. In practical terms, that means startups may raise capital differently, small businesses may access liquidity globally, and consumers may eventually interact with blockchain-based financial rails without even realizing it.

The projects that survive will likely be the ones focused on utility, governance discipline, security, and real economic participation. That is why I believe platforms like [Reaper Financial](https://www.reaper.financial/) deserve attention from long-term crypto investors rather than traders chasing short-term hype.

Build Bot-Resistant Market Intelligence

Much of the DeFi discussion is on the yield mechanics. Still, the biggest feature for long-term investors is sophisticated sentiment analytics, built to combat bot-driven market manipulation, because much of DeFi is social media-driven, and social listening that only quantifies volume and sentiment is completely useless when an AI bot network is manufacturing outrage and FUD.

The financial risk of coordinated manipulation is jaw-dropping, even when it happens against tradfi equities. (One example is that bot-driven outrage against a tradfi retail brand’s new logo caused their stock to drop 10.5%, erasing on the order of $100 million in a few days.) The WSJ finally reported that around half of the accounts engaged in that boycott were bots, and 70% of the posts at the peak of the attack were duplicated, i.e., the same message. If outraged bots can wipe $100 million off the valuation of a tradfi publicly traded company, the potential damage to hyper-reactive DeFi protocols is orders of magnitude bigger.

DeFi will start reshaping broader finance only when institutional investors and the DAO leadership build capabilities in bot detection, as part of their crisis management and investment strategy playbook. That is, they need to go beyond sentiment analytics as it currently exists and then reach out to specialist analytics firms, as some communications teams do with companies like Cyabra, to assess if the spikes of negative sentiment are actually coming from holders or if they’re coming from coordinated superattackers.

Before you pivot your protocol strategy or sell off your investors’ positions, your treasury and portfolio manager need to understand what they’re actually dealing with. Reacting to artificially generated FUD too quickly doesn’t just drive away real users; it trains other humanoid agents and algorithms to attack with more frequency and efficacy.

The best long-term crypto investors will be the ones who incorporate these additional lessons of DeFi analytics, who learn to analyze not just what is being said during a market moment, but who (or what) is actually saying it.

Leverage Restaked Pooled Security

Restaking is the development the DeFi clients we’ve worked with kept reorganizing their 2026 GTM around, because it was the first primitive in 3 years that pulled net new capital instead of recycling existing TVL between forks.

Across 7 protocol clients we ran positioning for, the ones who repositioned around restaked yield and shared security saw inbound from institutional desks roughly double inside one quarter, measured against their prior 6-month baseline. The reshape we observed was not retail-driven; it was treasury managers at funded protocols deciding where to park float, which is a different buyer with a longer attention span and harder questions. That buyer shift is what changed our content brief for crypto clients across the board.

Embrace Smart-Contract Liquidity And Escrow

In my three decades of watching traditional finance operate through a maze of middlemen and “gatekeeper” fees, the most promising development in DeFi is Automated Liquidity Provision and Decentralized Lending Markets. Specifically, the ability for an individual to act as their own “mini-bank” by providing liquidity to a protocol and earning a yield that isn’t eroded by a brick-and-mortar bank’s overhead.

For the long-term crypto investor, the promise lies in “Smart Contract Escrow.” In traditional law, escrow is a slow, expensive process involving third-party banks and manual verification. In DeFi, code is law. If Condition A is met, Payment B is released. This removes the “trust tax” we’ve been paying for centuries. It allows investors to put their digital assets to work—earning interest or providing collateral for loans—without ever having to ask a loan officer for permission or wait for a 48-hour wire transfer.

How does this reshape the landscape? It democratizes the “Yield Curve.” Historically, the most lucrative financial instruments were reserved for “accredited investors”—the folks who already have the most money. DeFi doesn’t care about your zip code, your credit score, or your last name; it only cares about the math in the smart contract.

However, a word of caution from a man who has seen every “sure thing” since the 1990s: decentralized does not mean “risk-free.” While the lack of a central authority is a feature, it also means there is no 1-800 number to call if the code has a “bug” or if you lose your private keys. DeFi will truly reshape finance when it bridges the gap between its current “Wild West” innovation and a more robust, legally recognized consumer protection framework. When that happens, the traditional banking model—which relies on keeping customers in the dark about how their money is being moved—will face its first real existential threat. It’s a shift from “Trust us, we’re a bank” to “Verify the code yourself.” That is a verdict the market is increasingly ready to deliver.

Prioritize Transparent Verifiable Protocols

DeFi isn’t my arena, but I’ll tell you what I’d actually want a crypto journalist to hear, because the most valuable thing in any emerging space isn’t the technology. It’s trust and discoverability.

Here’s my take that applies directly to DeFi: the development with the most long-term promise is transparency tooling. Whether it’s on-chain auditing, clearer protocol disclosures, or platforms that let investors verify claims instead of just believing them, that’s what separates lasting players from hype. I see the same pattern in marketing. Brands that win long-term aren’t the loudest; they’re the ones who back up their promises with proof.

DeFi will reshape finance the same way: by replacing “trust me” with “verify me.” The protocols that bake in measurable, provable performance are the ones serious investors should watch.

The other piece is discovery. A great protocol nobody can find or understand is worthless, same as a great website buried on page five of Google. As DeFi matures, the projects that explain tradeoffs clearly, educate their audience, and make complex value easy to grasp will pull ahead. We see it constantly: clients with solid offerings lose to competitors who simply communicate better.

So my advice to long-term crypto investors mirrors what I tell every small business we work with: chase substance over noise. Look for transparency, measurable results, and clear communication. The shiny thing fades; the trustworthy thing compounds. DeFi’s real promise isn’t in the next token, it’s in building financial tools people can actually verify and understand. That’s the foundation that lasts.

Related Articles

- DeFi’s Potential to Disrupt Traditional Finance: Expert Opinions

- Web3 and Decentralized Finance: Transforming Traditional Finance

- How Have DeFi Tools Revolutionized Investment Strategies?

You May Also Like

'Hypocrite': JD Vance gets more than he bargained for in testy appearance on ‘The View’

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

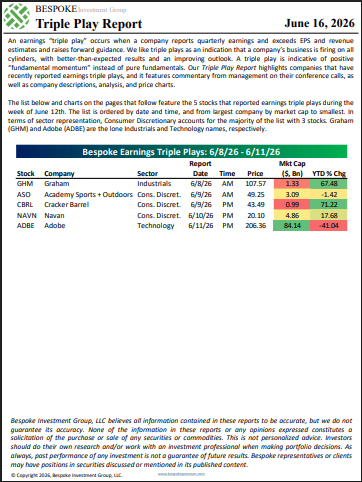

The Triple Play Report: 6/16/26