Oracle Stock Falls 43% From Its Highs Even as Its AI Backlog Hits $638 Billion

Key Stats for Oracle Stock

- 52-Week Range: $135 – $346

- Current Price: $140

- Street Target: $252

- TIKR Model Target: $483

- FY2026 Revenue Growth: 17%

- FY2026 Cloud Revenue Growth: 39%

- Remaining Performance Obligations: $638 billion, up 363% year over year

- FY2026 Free Cash Flow: negative $24 billion

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

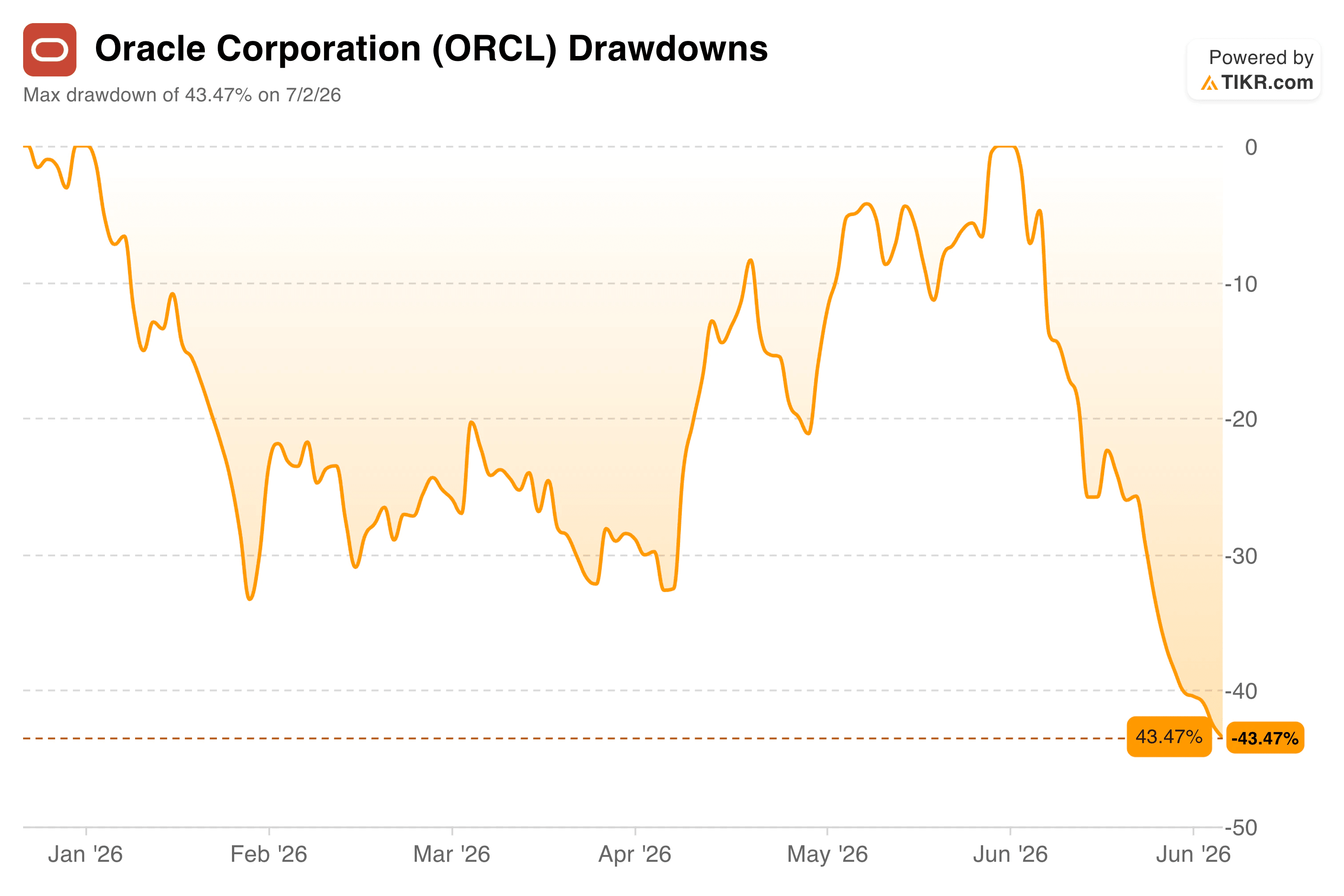

A 43% Drawdown Despite the Strongest Backlog Oracle Has Ever Reported

Oracle (ORCL) just closed out fiscal 2026 with numbers that would normally send a stock higher. Total revenue climbed 17% to $67.4 billion, cloud revenue jumped 39% to $34 billion, and Remaining Performance Obligations, the contracted future revenue sitting on Oracle’s books, surged 363% year over year to $638 billion.

That backlog grew by $85 billion in the fourth quarter alone, driven largely by large-scale AI infrastructure contracts.

Instead, the stock has fallen 43% from its 52-week high of $346, hitting a fresh low around $140.

Oracle Stock Drawdowns. (TIKR)

Oracle Stock Drawdowns. (TIKR)

The drawdown chart shows how this played out. Oracle spent most of the year churning through a series of drawdowns in the 15% to 35% range, recovering some ground each time, before a sharp final leg down starting in mid-June, which pushed the stock into its steepest decline of the year.

That last move came right after the fiscal fourth-quarter print, not before it, which suggests the sell-off isn’t a reaction to weak demand. It’s a reaction to the bill for meeting that demand.

See historical and forward estimates for Oracle stock (It’s free!) >>>

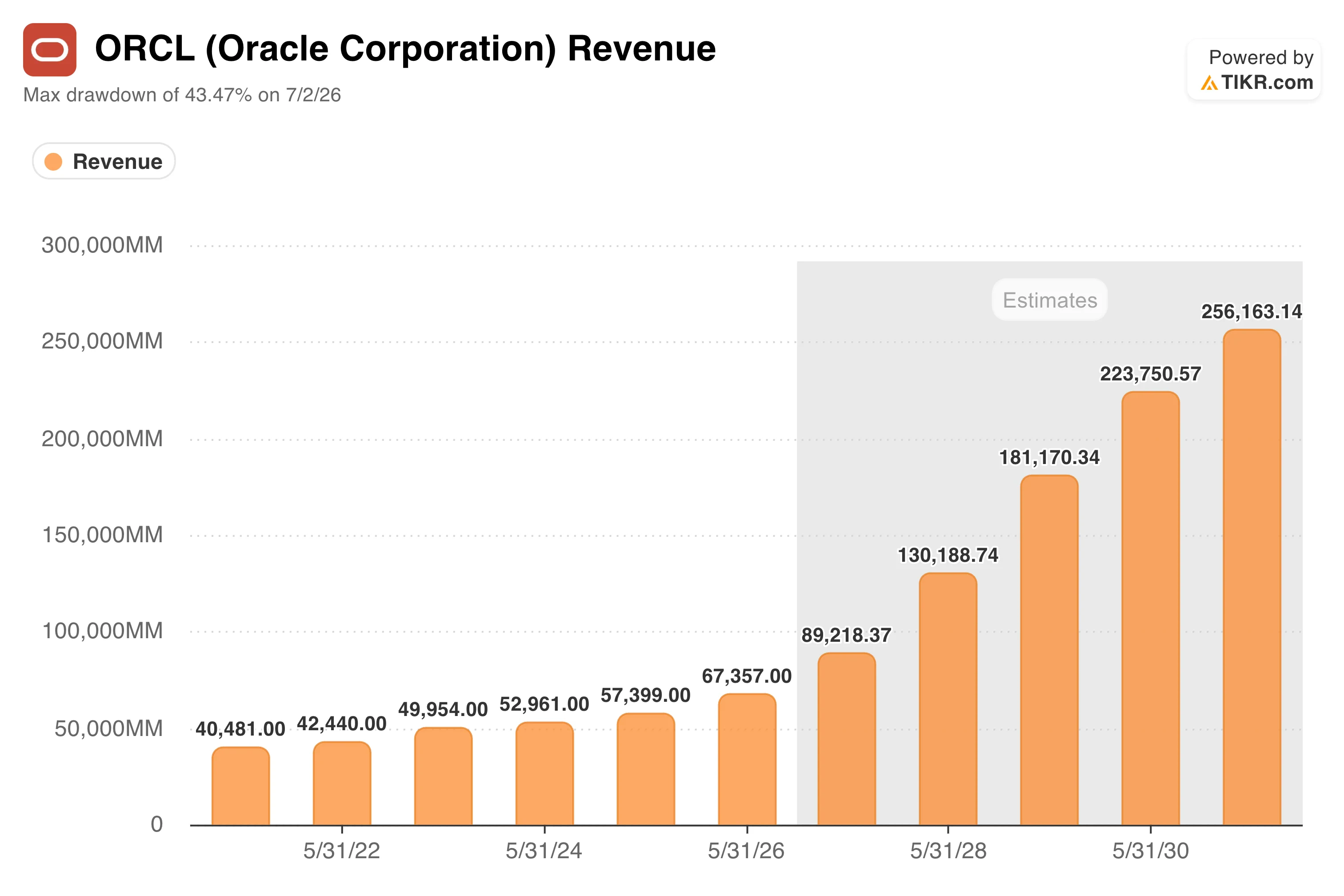

Why Revenue Keeps Climbing While the Stock Keeps Falling

To understand the disconnect, it helps to separate two different questions: is Oracle’s business growing, and can Oracle afford to keep growing it that way?

Oracle Revenue Estimates. (TIKR)

Oracle Revenue Estimates. (TIKR)

On the first question, the answer is clearly yes. Oracle’s revenue has climbed steadily from around $40 billion in fiscal 2022 to $67 billion in fiscal 2026, and TIKR’s forward estimates show that growth is accelerating sharply from here, with consensus projecting revenue near $130 billion by fiscal 2029 and continuing to climb toward $256 billion by fiscal 2031 as AI cloud contracts convert into recognized revenue.

That’s a meaningfully steeper slope than Oracle’s historical growth rate, reflecting just how much of the current backlog is expected to show up in the income statement over the next several years.

The second question is where the market has gotten nervous. Building the data center capacity to serve that backlog cost Oracle about $56 billion in capital expenditures this year, up 162% from the prior year, and pushed free cash flow to negative $24 billion, a sharp swing from a much smaller shortfall the year before.

To help fund the next phase, Oracle plans to raise around $40 billion in fiscal 2027 through a mix of debt and equity, including a $20 billion at-the-market share sale that would dilute existing shareholders.

Oracle’s debt load has already climbed past $130 billion. None of that means the demand is fake. It means Oracle is essentially pre-funding a buildout years ahead of the revenue it’s meant to support, and investors are being asked to trust that the timing works out.

See how Oracle performs against its peers in TIKR (It’s free!) >>>

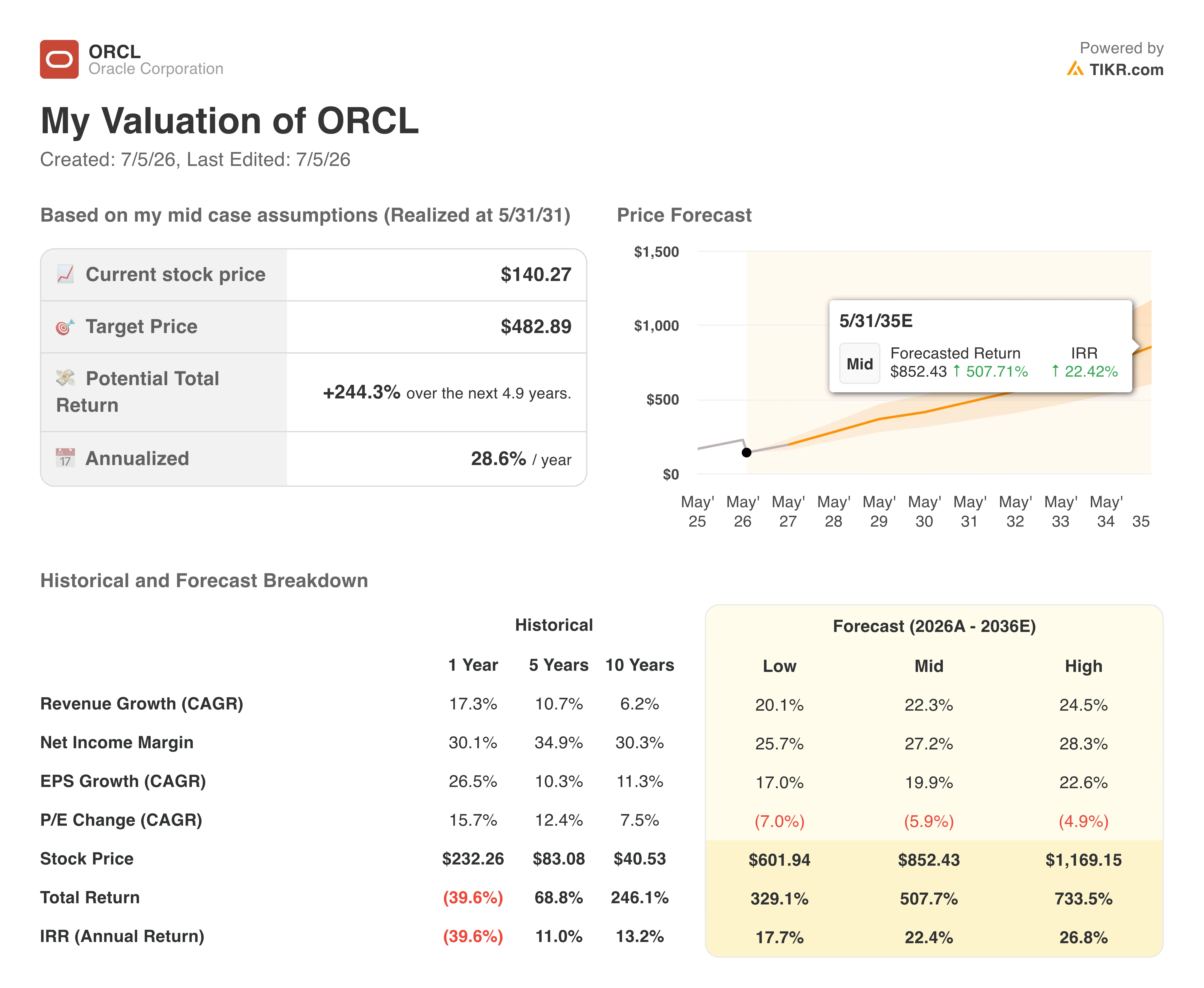

What Does the Valuation Model Say?

TIKR’s model uses a current price of $140 against a mid-case target price around $483, implying a potential total return of around 244% and an annualized return of around 29% over the next five years.

Oracle Valuation Model. (TIKR)

Oracle Valuation Model. (TIKR)

That target leans heavily on Oracle successfully executing the buildout it has already committed to. The mid case assumes revenue growth of around 22% annually, well above Oracle’s historical pace but roughly in line with what the current backlog implies, alongside net income margin expanding to around 27% as the cloud infrastructure business scales.

The model also assumes some multiple compression along the way, meaning the return isn’t dependent on the market re-rating Oracle back toward its old highs. It’s dependent on earnings growth doing the work.

The Street’s own consensus target sits meaningfully lower, at around $252, still implying solid upside from here but reflecting more caution about financing risk than TIKR’s model does. That gap is really about how much credit each framework gives Oracle for converting its backlog into cash without straining its balance sheet further.

Should You Invest in Oracle Corporation

Oracle’s selloff isn’t a story about fading demand. Revenue, cloud growth, and backlog are all at record levels, and the AI infrastructure buildout behind them is real and contracted, not speculative. The genuine risk is financing: rising debt, negative free cash flow, and a $40 billion funding plan that could dilute shareholders if it leans too heavily on equity. Investors willing to underwrite that execution risk are being offered a business growing faster than at almost any point in its history at a price well below where it traded a year ago.

See analysts’ growth forecasts and price targets for Oracle stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Ripple Price Analysis: What Are XRP’s Next Targets After 8% Weekly Surge?

Michael Saylor Says Bitcoin's Security Lies in Its Hard Consensus Model

TON Station Daily Combo 6 July 2026: Win SOON Points!