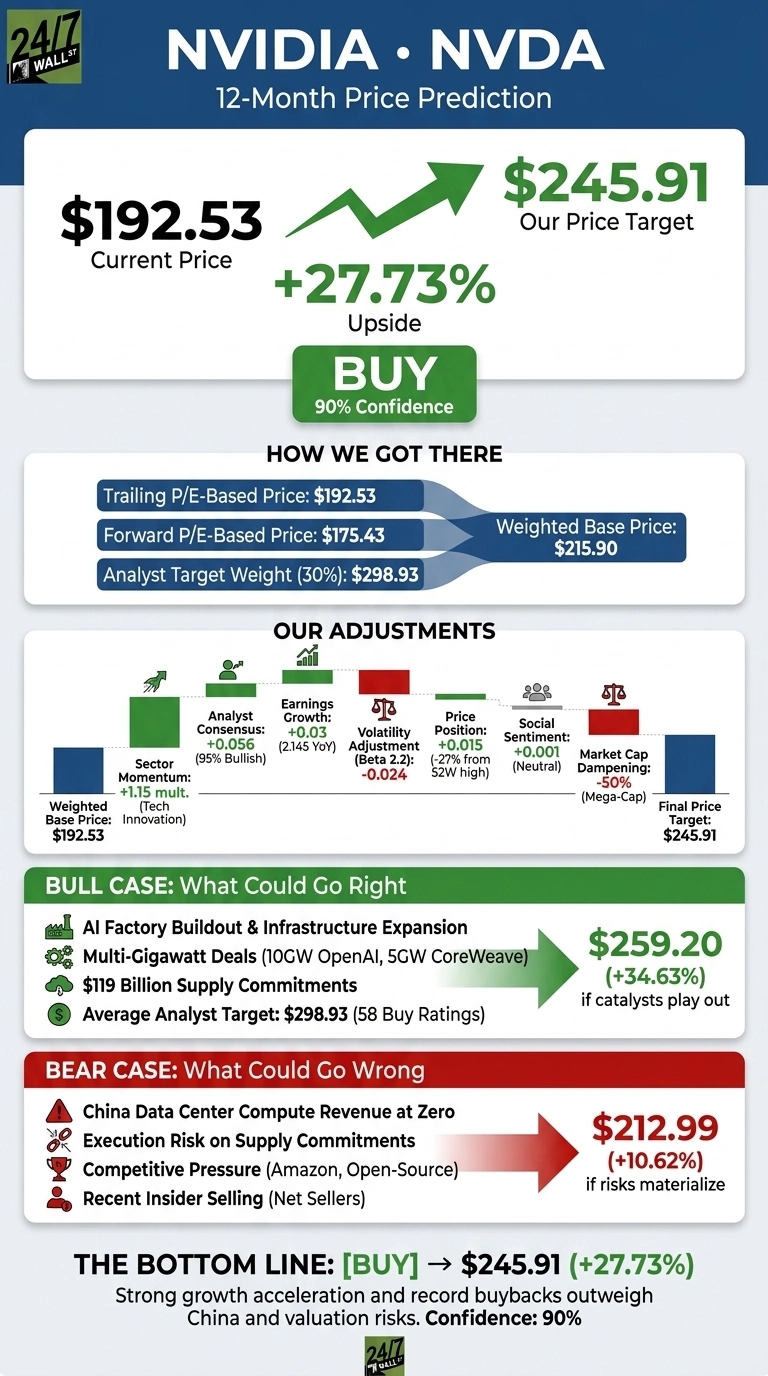

NVIDIA (NVDA) has become one of the most influential US stocks in the market because it sits at the center of semiconductor stocks, AI stocks, and data center infrastructure. Over time, NVDA stock price tends to follow a small set of fundamentals: earnings power, free cash flow, and the valuation multiple investors are willing to pay for them. NVDA can also swing sharply when expectations change, because the market often prices NVIDIA as a “high-growth infrastructure” company rather than a slow-and-steady cyclical chip name.

NVDA stock price performance and historical return pattern

NVDA has shown extreme upside in strong risk-on and AI-driven periods, and deep drawdowns when growth expectations or valuation compress. One practical way to set expectations for volatility is to look at annual total returns (dividends reinvested).

The table below uses one widely-followed total-return dataset (inflation-adjusted, dividends reinvested). It’s not a promise of what happens next, but it’s a clean way to understand how “normal” NVDA volatility can be compared with other mega-cap US stocks.

Year | NVDA total return | AMD total return | INTC total return | MSFT total return |

2020 | 119.32% | 97.31% | −15.84% | 40.62% |

2021 | 110.66% | 46.59% | −0.91% | 42.45% |

2022 | −53.29% | −57.72% | −49.88% | −32.40% |

2023 | 227.99% | 120.21% | 88.24% | 53.06% |

2024 | 163.67% | 20.36% | −60.69% | 9.76% |

2025 (YTD in dataset) | 37.96% | 73.02% | 75.47% | 13.3% |

Two takeaways usually matter for a trading or research mindset. First, NVDA stock price can move far more than the average large-cap stock, because it is often priced off forward AI infrastructure expectations. Second, NVDA can still be “right long-term” while being painful short-term, because multiple compression can overpower business momentum for extended stretches.

What drives NVDA stock price: the big drivers that repeat across cycles

Most explanations of what moves NVDA stock collapse into a few repeatable variables. The details change, but the drivers stay surprisingly consistent.

Earnings expectations are the core driver. If the market believes NVIDIA’s earnings power is strengthening, NVDA stock price tends to rise. If investors think demand is pulling forward and a digestion phase is coming, the stock can fall quickly even while current results still look strong.

Revenue mix matters because NVIDIA is not a single-market company. In recent years, Data Center revenue has become the anchor of the NVDA narrative. In NVIDIA’s fiscal year ended January 26, 2025, the company reported total revenue of $130.5B, with Data Center revenue of $115.2B, and operating income of $81.5B. That level of operating profit is one reason NVDA is often treated as “infrastructure-like” rather than a typical cyclical chip name.

Margins are a high-signal driver because they translate demand into earnings power. NVIDIA explicitly links margin changes to factors like mix (particularly the weight of Data Center), supply-chain costs, and inventory provisioning dynamics. When margins are stable or improving, the market is more willing to pay a premium multiple. When margins are pressured, the multiple can compress even if revenue remains high.

Valuation is the second major driver after earnings, and it often explains the biggest swings in shorter windows. NVDA is frequently priced as “future earnings times a premium multiple.” When interest rates rise, risk appetite weakens, or growth expectations cool, that premium can compress fast.

Customer concentration and capex cycles matter because a meaningful share of AI infrastructure demand comes from large buyers with lumpy purchase patterns. Even without naming every customer, the market often reacts to any sign that ordering is accelerating or pausing.

How to read NVIDIA earnings in a way that helps with NVDA stock price

A useful way to read NVIDIA results is to treat them as a set of repeatable checkpoints that link directly to NVDA stock price drivers.

Start by anchoring on the income statement scale and profitability. NVIDIA’s fiscal 2025 results show why the market focuses on earnings power: $130.5B revenue and $81.5B operating income is an unusually strong profitability profile for a company still being priced for growth.

Then connect the quarter to the forward narrative. The market typically reacts most to whether demand looks like a multi-year buildout or a short-term surge. This is where management commentary about supply, lead times, platform transitions, and the pace of deployment tends to matter more than headline “beat or miss” framing.

After that, treat margins as the “quality signal.” NVIDIA’s filings discuss how gross margin can be influenced by revenue mix, costs, and inventory effects, which is why margin commentary can move valuation quickly.

Finally, connect the story to capital return and reinvestment. NVIDIA reported fiscal 2025 net income of $72.9B and disclosed both share repurchases and cash dividends in its equity statement, which gives context for how the company balances reinvestment with shareholder returns.

Simple valuation tools for NVDA stock valuation

Most NVDA valuation debates sound complex, but they usually reduce to a few practical tools.

Earnings and multiple framing is the simplest: price follows what investors believe future earnings will be, multiplied by the P/E (or a similar earnings-based multiple) the market assigns. Bulls typically assume a strong earnings path and a premium multiple that holds. Bears usually assume earnings normalize faster than expected or the multiple compresses.

Multiple sensitivity is essential for NVDA. When a stock is priced for growth, a modest change in the multiple can translate into large moves. That is why NVDA can fall hard even if the business remains profitable, and why it can rally explosively when the market regains confidence.

Cash generation and reinvestment discipline matters because NVDA’s long-term value depends on whether it can keep converting AI demand into durable cash flow while sustaining leadership. NVIDIA’s fiscal 2025 profitability profile, including very large operating income, is one reason the market often treats NVDA as a premium compounder rather than a purely cyclical trade.

NVDA price prediction 2026 & 2030: a reusable scenario framework

A forecast becomes more useful when it is explicit about inputs. For NVDA price prediction 2026 and NVDA price prediction 2030, the cleanest reusable structure is to separate two building blocks.

The first building block is an earnings path (or net income path). The second building block is the valuation multiple the market assigns to those earnings.

Because share count can change with buybacks and stock-based compensation, a durable way to keep the math “update-friendly” is to forecast market cap ranges first, then translate to a per-share price using the share count you prefer (basic, diluted, or forward estimate).

Baseline anchor from filings: NVIDIA reported $72.9B net income for fiscal 2025.

Example scenario table for 2026 (market cap framework)

Scenario | 2026 net income assumption (illustrative) | P/E range (illustrative) | Implied market cap range |

Bear case | $60B to $75B | 18 to 24 | $1.1T to $1.8T |

Base case | $75B to $95B | 24 to 32 | $1.8T to $3.0T |

Bull case | $95B to $120B | 32 to 40 | $3.0T to $4.8T |

How to translate to a NVDA stock price range: take the implied market cap range and divide by the share count basis you are using. This is exactly why the framework stays evergreen: if earnings expectations rise or fall, you update the net income row; if rates and sentiment change, you update the multiple.

Example scenario table for 2030 (market cap framework)

Scenario | 2030 net income assumption (illustrative) | P/E range (illustrative) | Implied market cap range |

Bear case | $80B to $110B | 14 to 20 | $1.1T to $2.2T |

Base case | $110B to $160B | 18 to 26 | $2.0T to $4.2T |

Bull case | $160B to $230B | 24 to 32 | $3.8T to $7.4T |

What makes this structure credible is not the exact numbers, but the discipline of stating what must be true. Higher earnings power can justify a high outcome, but the market still has to “pay up” with a multiple. Conversely, even strong earnings can produce muted stock returns if the multiple compresses.

NVDA vs peers: return context and business reality

Peer comparison matters because NVDA often trades as a “lead indicator” for the broader AI infrastructure theme. On pure return behavior, the multi-year pattern is stark: NVDA’s strongest years can dwarf peers, and its weak years can still be brutal.

On fundamentals, NVIDIA’s latest annual profitability profile helps explain why it is priced differently. In fiscal 2025, NVIDIA reported $130.5B revenue and $81.5B operating income, which is an unusually high operating profit scale.

For contrast, Intel’s fiscal 2024 results show a very different operating reality in semiconductors: Intel reported $54.2B revenue and a GAAP net loss of $18.8B for the year.

This gap in profitability is why “NVDA vs INTC” is usually not just a product comparison, but a business-model and margin-structure comparison. “NVDA vs AMD” debates tend to be closer on positioning in accelerators and platform strategy, while “NVDA vs MSFT” comparisons often reflect ecosystem power and how AI monetization shows up in software and cloud economics.

NVDA and tokenized stock-style markets on MEXC: NVDAON and NVDAX

NVDA-linked price exposure can also appear on crypto platforms in tokenized or tracker-style formats.

NVDAON is shown on MEXC as an NVIDIA-linked market under the NVDAON/USDT trading page.

NVDAX is commonly presented as “NVIDIA xStock,” and product materials describe

NVDAx as a tracker certificate issued as Solana SPL and ERC-20 tokens designed to track the price of NVIDIA as the underlying.

In any comparison between NVDA stock and tokenized or tracker-style markets, the core distinction is structural. Holding NVDA through a traditional brokerage account is ownership of a share under the US market’s custody and shareholder-rights framework. Tokenized or tracker products can follow the price while using a different issuance structure, different settlement rails, and different risk and protection profiles, even if the price chart looks similar.

Common mistakes in NVDA stock price analysis

A common mistake is treating NVDA as a pure chart story and ignoring that the bigger multi-month moves usually come from changes in earnings expectations and the multiple.

Another mistake is assuming demand is either “permanently exponential” or “about to collapse.” Semiconductor infrastructure spending often moves in waves. The market usually prices NVDA off whether the next wave looks broader and more durable than the last.

A third mistake is using a single target price without stating assumptions. Scenario ranges tied to earnings power and valuation are usually more stable and easier to update.

FAQ: NVDA stock price and NVDA price prediction

What is a practical way to think about NVDA stock price?

NVDA stock price is often best framed as expected future earnings power multiplied by the valuation multiple investors are willing to pay. The market reacts most when something changes the earnings path or changes the confidence level in that path.

What tends to move NVDA the most around earnings?

Forward-looking signals about Data Center revenue, margin direction, supply and deployment pace, and whether demand looks broad-based or concentrated tend to move NVDA the most, because they change the market’s view of durability.

Why can NVDA fall even when NVIDIA is reporting huge revenue?

A decline often happens when the market compresses the valuation multiple due to rates, risk appetite, or a belief that growth is pulling forward. A strong business can still have a weaker stock outcome if the multiple resets.

How should NVDA price prediction 2026 and NVDA price prediction 2030 be presented?

A scenario framework is usually more durable than a single number. The useful version states assumptions about earnings power and the multiple, then translates the result into a market cap and a per-share range.

Are NVDAON and NVDAX the same as owning NVDA shares?

Not automatically. NVDAON and NVDAX are typically structured as tokenized or tracker-style price exposure on crypto platforms, and the structure, rights, settlement, and protections can differ from holding NVDA shares through a traditional brokerage account.

Disclaimer: This article is for educational purposes and general research. It is not financial advice or a recommendation to buy or sell any security or digital asset.

Disclaimer: This article is for educational purposes and general research. It is not financial advice or a recommendation to buy or sell any security or digital asset.